Doc's Daily Commentary

Mind Of Mav

Crypto Is Eating Fintech: The Future Of Finance As We Know It

Ten years ago this past August, Marc Andreessen stated that software was eating the world. Almost two years ago, Angela Strange, general partner at Andreessen Horowitz, suggested that every company will become a fintech company.

The first of these proclamations has become inarguably true; the second appears to be on a similar path. Software companies are increasingly embedding banking into their services and an explosion of financial tools are penetrating B2B product offerings as companies recognize that financial services can serve as a powerful stimulant to their existing network effect flywheel. The next phase of this evolution is becoming impossible to ignore: if every company becomes a fintech company, then it seems inevitable that those same companies will become crypto companies, in that a significant portion of revenue and user engagement will be driven by crypto products and the underlying infrastructure used to facilitate financial transactions will be crypto-native. We have seen this first in how the productization of crypto has permeated consumer fintech platforms, with the larger and more disruptive trend of crypto-networks powering the future of all financial services looming on the not-so-distant horizon.

The combination of developing Web3 financial services infrastructure and growing consumer demand for digital assets is pushing all companies that interact with financial technology to crypto. Crypto-networks and crypto-assets will become the common denominator connecting wallets and financial services globally, driving significant revenue generation and user engagement for consumer-facing platforms and facilitating more efficient B2C and B2B financial interactions relative to the legacy financial system.

Crypto is a Product, and Everybody Wants It

Crypto as Fintech’s Monetization and Engagement Engine

Growing consumer demand for crypto-assets is pushing both fintechs and incumbent financial services firms to productize crypto-assets. Offering users access to crypto-assets is no longer differentiating — it has quickly become table-stakes: in Gemini’s 2021 State of U.S. Crypto Report, 77% of those surveyed either own crypto or consider themselves “crypto curious.” And fintechs should want to add crypto to their platforms, as it is quickly becoming a significant source of user acquisition and engagement.

The best example of this is Square, a company that began its lifecycle as a point-of-sale solution for SMBs and has since become a corporate leader in providing consumers access to bitcoin. Since launching bitcoin purchases via Cash App in late-2017, that product line has grown to a $10+ billion revenue run-rate. This has supercharged Cash App’s monetization, user acquisition, and app engagement: Cash App now has almost 40 million monthly active users, up from 7 million in late-2017, pushing rival Venmo to launch a similar product offering in 2020 as a response.

Robinhood was another relatively early mover in offering a crypto-asset product line, launching Robinhood Crypto in 2018. Since then, Robinhood has become a company driven by (and reliant on) crypto: in the two quarters since its IPO in early 2021, Robinhood has generated $233 million and $51 million in revenue from crypto transactions, respectively — up from $5 million in Q2 2020. Crypto has accounted for ~40% of transaction-based revenue since IPO, up from 4% in Q4 2020. The firm now holds more than $20 billion of crypto assets on the platform. Revolut, one of Europe’s largest neobanks and another early mover into crypto, has also seen significant growth from crypto, as crypto assets held on the platform grew more than 5x in 2020 to $742 million.

Interest in crypto is relevant to employers, too. As Nikhil Trivedi points out in his next big thing issue #37, crypto businesses and product line teams have become a magnet for the best talent. This is in part the result of a maturing ecosystem, as leading crypto-native companies now have the resources and needs to build out robust engineering, financial, operational, legal, and business-related functions. But crypto’s growing gravitational pull on high-quality talent is being fundamentally driven by the realization of its multidisciplinary promise. There is room for innovation and appeal to individuals across a wide array of disciplines — computer science, cryptography, game theory, community-building, economics, finance, culture, media, gaming, etc. — giving crypto-related teams a significant leg up in attracting talent across industry lines. In the war on talent, crypto companies now offer world-class compensation and a front row seat to the broadest and deepest technology innovation today.

Social Platforms Look to Stay Ahead by Launching Crypto Features

Social media platforms have enormous reach, touching roughly 4 billion people globally. They sit at the center of modern culture and are now embedding financial services to engage with users more deeply, making them obvious candidates to integrate crypto-assets and -networks. We are beginning to see how these integrations can both supercharge their financial services efforts and create opportunities for new features not previously feasible using the traditional financial grid.

Twitter’s recent announcement that they are enabling tipping with bitcoin, making it the first major social network to encourage use of bitcoin as a method of payment, is a perfect example. Bitcoin’s Lightning Network, a protocol built on top of Bitcoin that is designed to enable faster and cheaper transactions, provides the solution to efficiently scaling micro-payments that hasn’t existed before.

Similarly, Reddit is looking to expand its Ethereum-based crypto token rewards program for community members after launching a testing phase in 2020. Users can earn the tokens by submitting quality posts and comments, allowing them to act as a measure of reputation within the community — baking in consequence and monetization into the quality of a user’s engagement with the platform. And because they exist on the Ethereum blockchain, they can be used in other Ethereum-based applications.

Tipping and community-based rewards are relatively innocuous features on their own, particularly given the small scale at which they exist today. However, they foreshadow the continued blurring of the line between social and finance. These early forays into crypto-powered product features offer a glimpse into what could come next, from communities monetizing their cultural reach to individual brands becoming investable assets. As community platforms become hubs for small businesses and digital identities, crypto will play a meaningful role in these seamless social-financial interactions.

Web3 Infrastructure as the Financial System’s Backbone

While crypto is becoming a significant user acquisition and revenue generation tool for consumer-facing platforms, its importance to the future of financial services is best captured in how it is transforming the financial grid at its core. Today’s financial infrastructure, even that used by leading fintech companies, largely uses fundamental technology that was built almost 50 years ago. The first meaningful wave of fintech startups has built services on top of and around legacy systems. The opportunity available to the open system of finance that is being built on crypto-networks today: to become the backbone for all financial services going forward, creating new business models and driving a step-function improvement in user experience.

We are already seeing traditional financial services companies adopt crypto’s “tech stack” as they recognize the potential of cheaper, more efficient payment rails and open access to financial products. Visa announced earlier this year that they will begin piloting transaction settlement in stablecoins on the Ethereum blockchain. Visa’s interest in tapping a leading crypto-network to be the foundation for transaction settlement is notable. Though this remains a pilot program today, Visa’s involvement validates the growth of stablecoins, an asset class that has grown from less than $1 billion in 2019 to more than $100 billion today because of its interoperability with open financial applications and fast, cheap settlement capability, and the technical infrastructure on which they exist.

Shortly after the Visa news became public, the European Investment Bank (“EIB”), one of the largest supranational lenders in the world, launched a digital bond issuance on the Ethereum blockchain. The EIB highlighted the benefits that crypto-network-based financial services may bring to market participants, including the reduction in fixed costs and reliance on intermediaries, better market transparency into capital flows and asset owners, and much faster settlement speed.

The adoption of crypto-network infrastructure by financial services giants remains in its early stages but the actions of Visa and the EIB likely foreshadow how crypto-networks will permeate the financial ecosystem and become the foundation on which seemingly traditional financial applications, services, and business models reside. It is difficult to see how an overwhelming percentage of digital transactions do not move onto the crypto tech stack; everything from stocks to bonds to real estate transactions will touch crypto at the settlement layer. Put simply: financial services will increasingly run on crypto-networks going forward.

A New Financial Stack Means Business Model Innovation…

A crypto-network-based financial grid not only carries benefits for existing financial services but allows for new business models entirely. The efficiencies provided to applications built on top of crypto rails and the composability enabled by tokenization allow users access to product features (and teams the ability to build product platforms) that aren’t possible within traditional business models. The result is an ecosystem of financial building blocks free of fee extraction from middlemen and human biases at the point of transaction, and available for anyone on which to build or integrate. We have already seen significant product-market fit in areas like peer-to-peer lending, where the two largest lending protocols today — Aave and Compound, both founded in 2017 and which launched within the last three years — combine to have more than $15 billion in loans outstanding and have generated more than $600 million in annual revenue.

Furthermore, building on top of crypto-networks makes products globally accessible and cross-platform composable by default, fundamentally changing how platforms reach end users and integrate with other protocols (similar to how traditional companies today partner with others for product distribution). The elegance of this composability is that it enables access to financial tools with just a few lines of code, allowing one innovation to unlock dozens of others and streamlining the building of local, national, and international businesses on top of smart contract-based protocols. Aave offers a prime example for what composability can unlock: by integrating with multiple applications, it can offer users access to “flash loans” — a product that lets users borrow tokens without collateral, put the loan to use in an integrated application, and pay back the loan, all in one transaction.

The transformative potential of this lies in how it can extend the reach of financial services to underbanked communities and allows “non-financial” platforms to easily embed financial services into their ecosystems. We are already seeing this with the emergence of play-to-earn platforms like Axie Infinity, and we should expect further integration of these ‘money legos’ into historically non-financial platforms.

…and Better User Experiences

Technical advancement often outpaces user experience when building on the frontier edge of innovation. Crypto is no different — securely interacting with crypto applications via mobile is almost non-existent and even desktop interactions often require a multiple-step process in confirming the right fees to pay and completing transactions. On the surface, crypto still has plenty of runway for experience improvement.

However, as crypto protocols increasingly integrate into easy-to-use aggregator platforms and mobile application functionality begins to emerge, the “hidden” user experience benefits at the core of crypto’s innovation come to the forefront.

Many startups have been founded on the idea of expanding accessibility to financial services to all; until bitcoin delivered the blueprint for distributed systems, the achievement of those goals was never realistic. Crypto-networks make financial services available to anyone in the world with internet and smartphone access — 4.7 billion and 6.3 billion people, respectively. These open networks lower the barriers to entry for entrepreneurs to effectively zero, as any person or business can leverage the transparent codebase and public APIs provided by existing open protocols to build financial products. The result is a slew of benefits for the user, with select examples shown below:

Crypto protocols enable instant, cheap, global transactions 24/7 while allowing users continuous access to and custody of their holdings.

Moving capital between platforms becomes trivial — it can be done at any scale in minutes, rather than facing transaction limits and multi-day settlement periods — forcing competitive iterations on fees and new products. This type of open competition will enable a step-function improvement in the rate of innovation for these financial services. Centralized platforms have notoriously seen user experience deteriorate as they scale and rely more on network effects than continued innovation for success.

Aligning incentives via trustless, programmable escrow-like accounts allows protocols to programmatically enforce insolvency, defaults, interest payments, etc., freeing users from traditional counterparty risk. The auditable nature of application codebases provides for “transparent accounting,” such that users can understand a product’s functionality and a platform’s quality of collateral and existing leverage in real-time.

As new business models emerge, so too will better products and improved user experiences. The next phase of this evolution will be the emergence of businesses built on crypto-network infrastructure and present a functional, easy-to-use experience like that which we have grown accustomed to from the consumer-facing businesses of the last decade. In several years, crypto will power the most innovative financial and social products and a meaningful portion of global financial transactions, and we won’t even realize it.

Despite the maturation of the crypto ecosystem and the emergence of new, potentially transformative business models, there remains meaningful regulatory risk as this rapidly evolving financial system has become a focus area for governments and regulators. Policymakers have varied in their approach to understanding and action, creating uncertainty as to how (and if) current-day technological innovation can be regulated using legal frameworks from the 1930s. The regulatory environment will remain volatile in the short-term, though the growing number of allies in government and increasing awareness of the benefits of crypto-enabled financial services throughout regulatory bodies provides optimism longer-term.

The ReadySetCrypto "Three Token Pillars" Community Portfolio (V3)

Add your vote to the V3 Portfolio (Phase 3) by clicking here.

View V3 Portfolio (Phase 2) by clicking here.

View V3 Portfolio (Phase 1) by clicking here.

Read the V3 Portfolio guide by clicking here.

What is the goal of this portfolio?

The “Three Token Pillars” portfolio is democratically proportioned between the Three Pillars of the Token Economy & Interchain:

CryptoCurreny – Security Tokens (STO) – Decentralized Finance (DeFi)

With this portfolio, we will identify and take advantage of the opportunities within the Three

Pillars of ReadySetCrypto. We aim to Capitalise on the collective knowledge and experience of the RSC

community & build model portfolios containing the premier companies and projects

in the industry and manage risk allocation suitable for as many people as

possible.

The Second Phase of the RSC Community Portfolio V3 was to give us a general idea of the weightings people desire in each of the three pillars and also member’s risk tolerance. The Third Phase of the RSC Community Portfolio V3 has us closing in on a finalized portfolio allocation before we consolidated onto the highest quality projects.

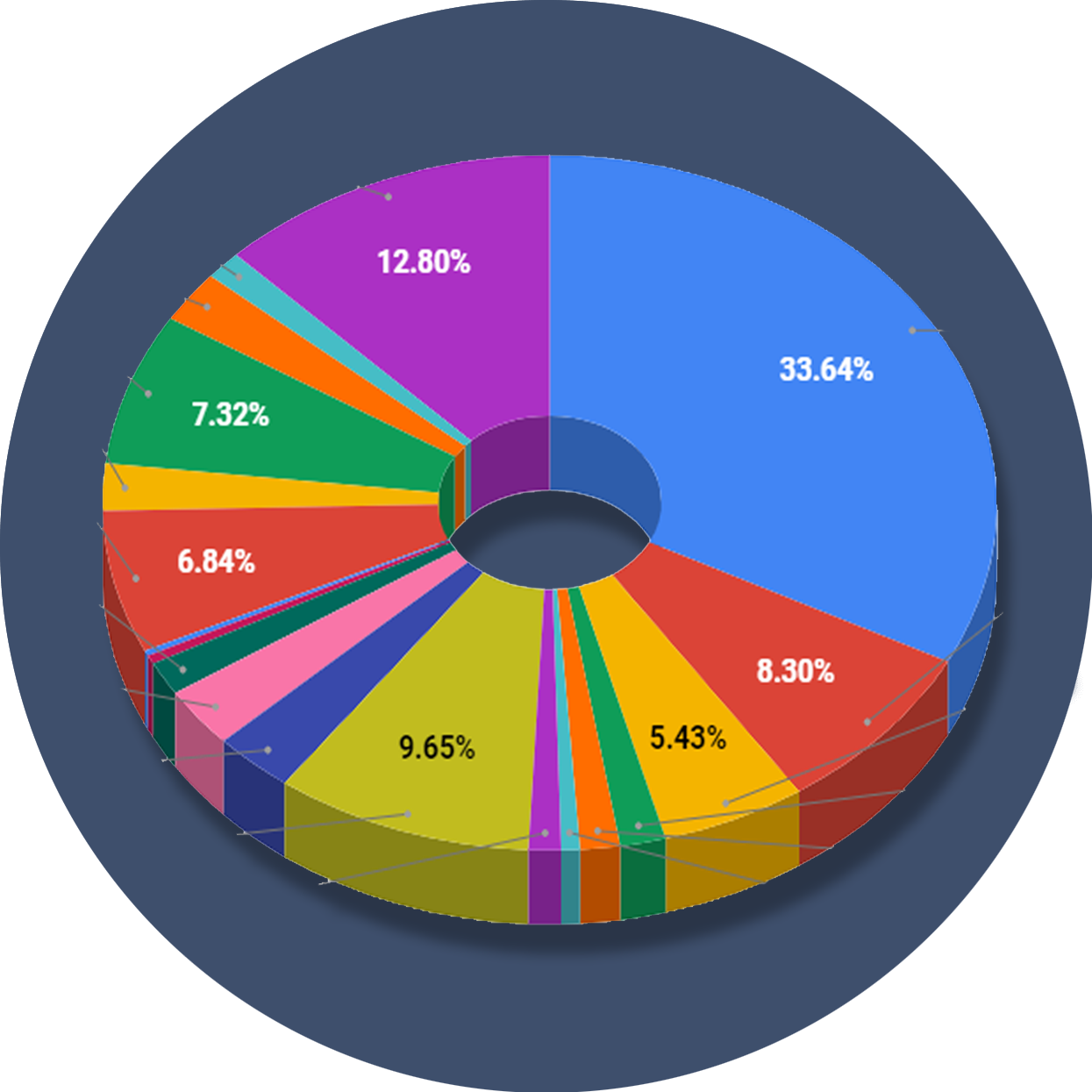

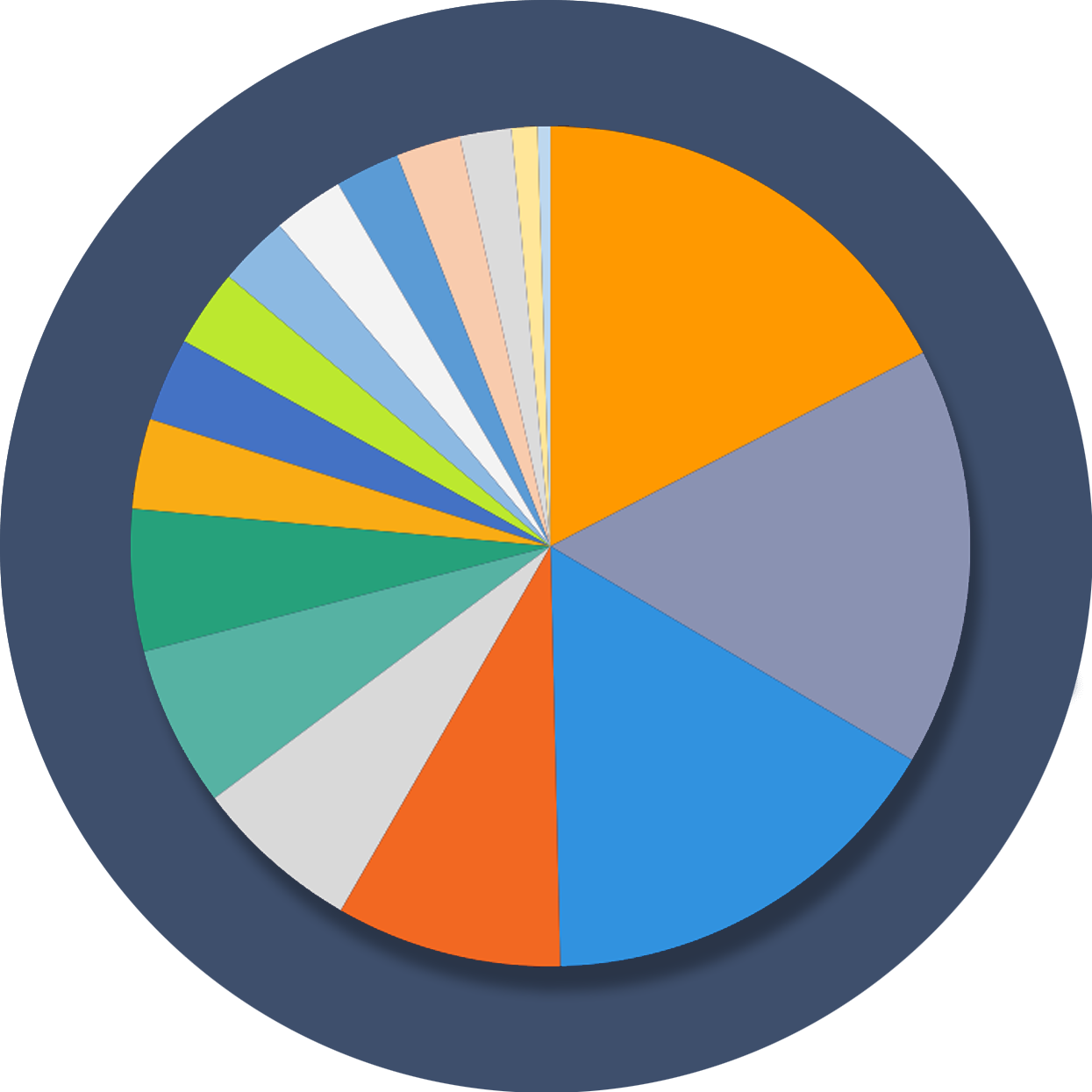

Our Current Allocation As Of Phase Three:

Move Your Mouse Over Charts Below For More Information

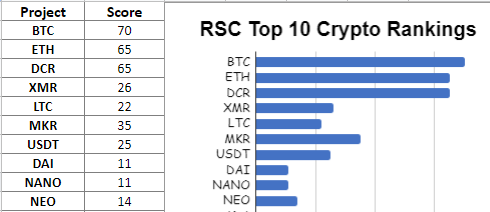

The ReadySetCrypto "Top Ten Crypto" Community Portfolio (V4)

Add your vote to the V4 Portfolio by clicking here.

Read about building Crypto Portfolio Diversity by clicking here.

What is the goal of this portfolio?

Current Top 10 Rankings:

Move Your Mouse Over Charts Below For More Information

Our Discord

Join Our Crypto Trader & Investor Chatrooms by clicking here!

Please DM us with your email address if you are a full OMNIA member and want to be given full Discord privileges.