Doc's Daily Commentary

Mind Of Mav

The Future of Money As We Know It

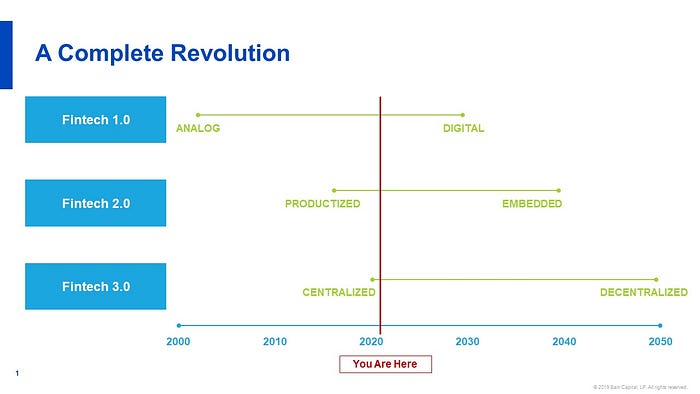

If you were looking into fintech companies in 2000, there was one main idea: that an analog sector would eventually become digital. The potential was obvious: here was a multi-trillion dollar industry, filled with atoms (think bank branches, paper documents, human labor, etc.), when all it ever needed was bytes. The transition to digital has and will reduce the friction and transaction costs of buying and using financial services, ultimately to zero.

Perhaps five years ago, the next leg of the journey became obvious. Once financial services were digital, they no longer needed to exist as discrete products; they could become embedded in software that consumers and businesses use all day long, and with which they have a durable and data-rich relationship. We are early in that process, and it requires imagination to see where it ends. For a while, it’s just going to feel like everyone we do business with wants to offer us a debit card, make us a loan or help us save 15% on our car insurance.

Eventually, though, when these products and services are all fully digital and embedded, the cognitive load of opening and managing these accounts will go away, as the operations are executed and automated by the software in which they are integrated.

Even more recently, with the mainstreaming of crypto and Web3, the final piece of the puzzle has snapped into place: over the next 30 years, financial services will go from centralized to decentralized, completing the revolution.

One reason that we have such fixed notions of what financial services can be is because of their analog history. When a product or service has high frictional costs, it leads to standardization, a phenomenon we have seen in other industries. When automotive manufacturing went from primitive industrialization to modern factories, we went from the Model T in just one color to infinite combinations of automobile makes, models, and features.

But another reason is that financial services is highly centralized, and the rules of the road are established and maintained by regulators, financial institutions, and their collective associations. Your debit card is built on the back of and fixed in place by DDA regulations, debit card switching network agreements, ATM standards and specifications, negotiated and regulated interchange schemes, etc. And that’s for a relatively risk-free product; the strictures on what your mortgage can look like make your debit card look like a party animal.

When your money instead lives in a set of cryptographically secure wallets, the full flower of human imagination can be brought to bear in determining the potential of those accounts.

For this digital, embedded, and decentralized world to reach its full potential, there are meaningful problems to be solved. We must be able to establish identity, at point of transaction and over time, even if pseudonymous. We must have real time and persistent credit risk management, for people, businesses and for specific obligations between and among them. We must have reliable cryptographic security, in a world without central counterparties to resolve disputes. We must solve money’s supply chain problem, requiring robust and time-tested capital allocation algorithms, so that excess liquidity in one place can be a source of liquidity elsewhere, in real time.

Once identity is solved, credit risk becomes easier. You can’t commit fraud or default on your debt just by wriggling free into the ether; your credit history is immutable and follows you everywhere. In a fully transparent world — even if pseudonymous — willingness to pay becomes a given, and so the analysis can focus on ability to pay.

In a fully liquid world, where capital comes from billions of individuals, businesses, and institutions, intermediated by hundreds of allocation protocols, people will no longer have liquidity problems. All their assets and future cash flow streams can be evaluated and the value time-shifted to them instantly, 24/7.

They can still, of course, have net worth problems, but increasingly money will be a probabilistic cloud. What is a better estimate of your financial worth: the balance of your bank account, or the present value of your future earnings? Those earnings obviously have different levels of certainty. Increasingly, you can get access to your already-earned wages. Why not the wages you’ll earn next week, with only slightly higher expense? Where does that end?

Depending on the discount rate of your future earnings, is that probabilistic money better kept as future earnings (yielding nothing), or invested in a solar array in Ghana? What steps can you take to inflect the curve of those future earnings? As you sit here today, reading this, is your actual net worth going up because of the power of these ideas? (That last one is strictly rhetorical; obviously, the answer is yes.)

The transition from an analog, productized and centralized industry to a digital, embedded and decentralized one — underpinned by advances in identity, risk management, information security, and the globalization and atomization of liquidity — leads to an industry characterized by automation, abundance and creativity, displacing the friction, cognitive load, and conformity of the past. We will have financial relationships with all our commercial counterparties; we will have nearly as many wallets as we have transactions.

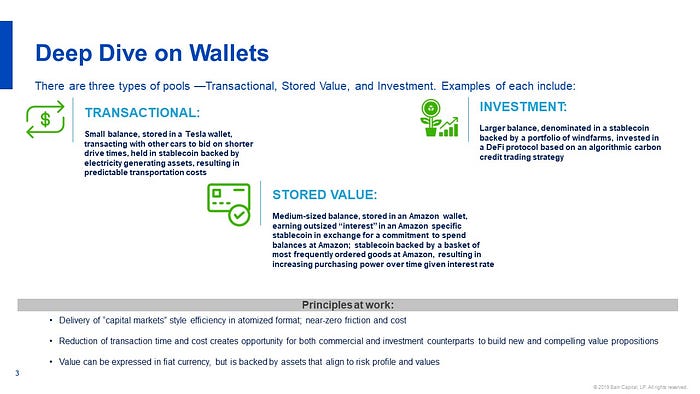

So let’s turn to those wallets. Merchants of all types will present customers with two main options: store money with me and I will reward you, or pay me later with little/no expense. As a consumer moves through their commercial life, he or she will constantly be flipping back and forth between net borrower or lender to their counterparties, depending on other calls on their capital and the quality of the deals on offer.

A consumer could, if pressed, verbalize their current situation or characterize changes to it — e.g., “I just swept all my merchant balances and will leverage BNPL offers for the next three weeks, while also pulling down my next quarter’s wages, so that I can allocate capital into the Latin American transportation sector given a short term outsized return there.”

But these choices will generally not be overt or even conscious. Smaller merchants, similarly, will not have sophisticated treasury teams managing their liquidity and structuring these offers; algorithms, protocols and global pools of liquidity serve as their back office, as well.

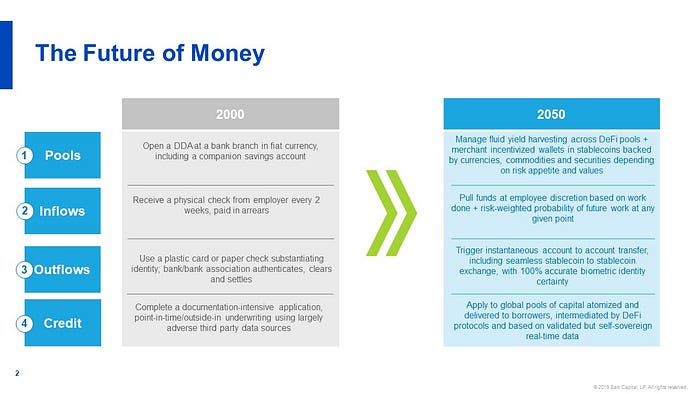

Which leads to the next question: what’s in those wallets? By 2040, we will be done with the bad trade that is fiat currency, where we give our capital for free to various governments for the privilege of having it diluted by the tax of inflation. Rather than our current conception of money — a token that is a representation of an entry in a central bank ledger — our assets will be 100% invested at all times, and we will shift those assets around between and among counterparties, who can instantly (and without cost) shift between various stablecoins.

As noted, money has historically had a supply chain problem in an analog, productized and centralized world, causing us to store it in various expensive and inefficient depots around our lives; in the future, money will be Just-In-Time.

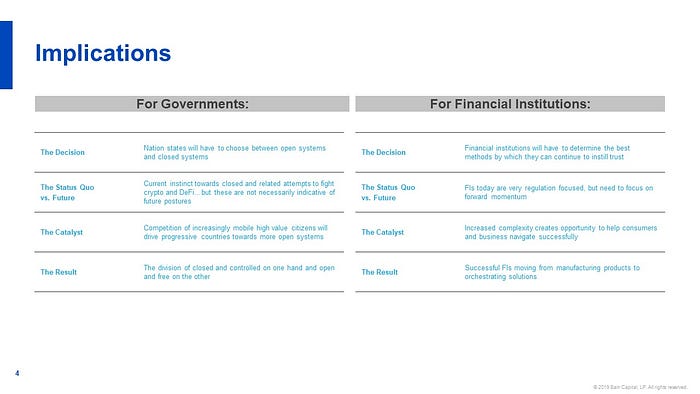

What are governments and banks to do about it? As we are seeing now, the first instinct of governments will be to wield sovereign power to retain their prerogatives; the first instinct of banks is to leverage regulatory capture to retain theirs. Eventually, it will grow more nuanced. Some countries will pursue open strategies — at first smaller countries, but hopefully over time the United States, as well.

Many will perceive Web3 as the enemy forever. This distinction will, over time, create a new Cold War. Banks have a real opportunity in this new world, as well, to provide the underlying rails in certain cases, and the curation and navigation layers, for those truly progressive institutions who are first to acknowledge and embrace decentralization. Those who are late to embrace this revolution will simply go away or be nationalized.

Venture capital investing in fintech has gone nuts lately. It looks like the industry will invest over $50B in private fintech companies this year alone, which will mean a three year total of over $100B. How can that make sense? Of course, perhaps it doesn’t; there is exuberance everywhere, and maybe it’s simply a bubble.

But let’s look at another big number: $800B. That’s the annual net income of the global financial services industry. At mean S&P PE multiples, that’s worth $12 trillion of enterprise value. I’ve come to believe that this is the size of the prize, and if you believe that, the investment levels can make sense.

Increasingly, fintech isn’t just about stealing the incremental customer, or participating in the evolution of the industry from analog to digital. It is a fundamental overthrow of how things have been done historically: a complete revolution.

The ReadySetCrypto "Three Token Pillars" Community Portfolio (V3)

Add your vote to the V3 Portfolio (Phase 3) by clicking here.

View V3 Portfolio (Phase 2) by clicking here.

View V3 Portfolio (Phase 1) by clicking here.

Read the V3 Portfolio guide by clicking here.

What is the goal of this portfolio?

The “Three Token Pillars” portfolio is democratically proportioned between the Three Pillars of the Token Economy & Interchain:

CryptoCurreny – Security Tokens (STO) – Decentralized Finance (DeFi)

With this portfolio, we will identify and take advantage of the opportunities within the Three

Pillars of ReadySetCrypto. We aim to Capitalise on the collective knowledge and experience of the RSC

community & build model portfolios containing the premier companies and projects

in the industry and manage risk allocation suitable for as many people as

possible.

The Second Phase of the RSC Community Portfolio V3 was to give us a general idea of the weightings people desire in each of the three pillars and also member’s risk tolerance. The Third Phase of the RSC Community Portfolio V3 has us closing in on a finalized portfolio allocation before we consolidated onto the highest quality projects.

Our Current Allocation As Of Phase Three:

Move Your Mouse Over Charts Below For More Information

The ReadySetCrypto "Top Ten Crypto" Community Portfolio (V4)

Add your vote to the V4 Portfolio by clicking here.

Read about building Crypto Portfolio Diversity by clicking here.

What is the goal of this portfolio?

Current Top 10 Rankings:

Move Your Mouse Over Charts Below For More Information

Our Discord

Join Our Crypto Trader & Investor Chatrooms by clicking here!

Please DM us with your email address if you are a full OMNIA member and want to be given full Discord privileges.