Doc's Daily Commentary and Watchlist

Mind Of Mav

Why Doesn’t The Fed Just Hike 200bps At Once?

The Federal Reserve is meeting this week, and everyone expects them to hike interest rates again, in order to control persistently high inflation. The consensus forecast is for a 75 basis point (0.75%) hike, though some have talked about going as high as 100bp. The former would bring the federal funds rate up to 2.5%, while the latter would make it 2.75%.

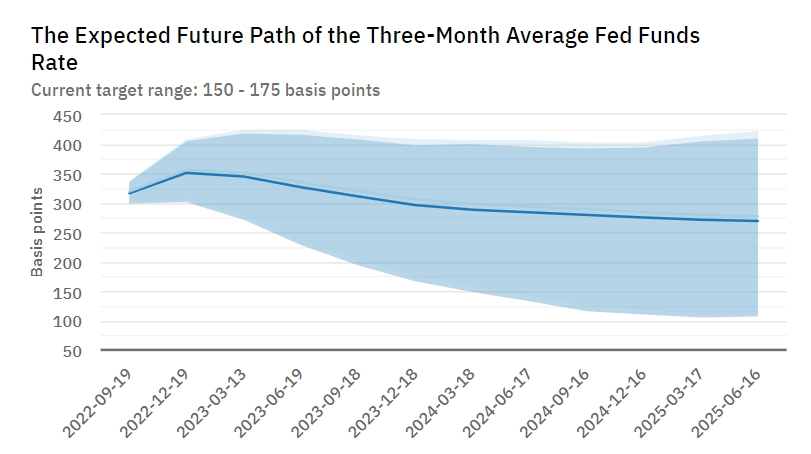

What’s interesting, though, is that markets expect the Fed to keep hiking after that. Here is the Atlanta Fed’s measure of market expectations for interest rates over the next few years. You can see it peaks at 3.5% (350bp) in December of this year:

What’s more, the Fed itself says it expects to hike rates more. Current “dot-plot” projections by Fed officials predict that rates will peak at around 3.8% in 2023.

So that raises the question: Why not just hike 200bp right now, in July, and get it over with? If you think 3.5% or 3.8% is where rates need to be, why not just go there right now?

Surprisingly, this is a question macroeconomists don’t think about a lot. Most macro models don’t say anything about raising rates gradually — they just specify the “optimal” level of interest rates. But this is simply the way those models are set up — the modelers decided to model the economy as responding to the level of interest rates, rather than their rate of change. That doesn’t mean that theory tells us we should raise rates quickly; it just means macroeconomists haven’t thought about this question much.

In fact, a few have thought about it. It’s a pretty well-established fact that the Fed does tend to change interest rates slowly and gradually; researchers have noted this for a long time. And some theorists have made models showing why this behavior might be justified.

For example, Mike Woodford — possibly the most influential macroeconomist in recent decades when it comes to monetary policy — has a 2002 paper entitled “Optimal Interest-Rate Smoothing”. Here’s the argument in typically dense Woodford-ese:

The essential insight into why interest-rate smoothing by a central bank may be desirable is provided by a suggestion of Goodfriend (1991), also endorsed by Rudebusch (1995). Goodfriend argues that output and prices do not respond to daily fluctuations in the (overnight) federal funds rate, but only variations in longer-term interest rates. The Fed can thus achieve its stabilization goals only insofar as its actions affect these longer-term rates. But long rates should be determined by market expectations of future short rates. Hence an effective response by the Fed to inflationary pressures, say, requires that the private sector be able to believe that the entire future path of short rates has changed.

The basic argument is about expectations. If the Fed raises rates really suddenly, it may convince people that even more rate hikes are on the way. So if the Fed were to hike rates by 200bp this week, it might not be interpreted as “OK we did 200bp, now let’s wait and see what happens before hiking more”. It might be interpreted as “We’re going to 8%! Woohoo!!” In which case the economy might overreact and crash.

This isn’t the only reason the Fed might want to go slow. Sack & Weiland (2000) argue that uncertainty and measurement error regarding macroeconomic variables (growth, inflation, etc.) mean the Fed needs to be cautious because it doesn’t actually know exactly what’s happening to the economy.

(Side note: There are also some arguments that interest rate smoothing promotes financial stability, though some say it actually hurts financial stability. And there are some very theoretical arguments that I don’t take very seriously, because they rely way too much on fairly arbitrary characteristics of simple models that no one actually believes. So I’m sticking with A) expectations, and B) uncertainty about the economy as the most important reasons to smooth interest rates.)

Arguments for rapid, bold rate changes are less common in the academic literature. But again, this might just be because of the way academic econ works. Economists have a tendency to tell just-so stories — they look at the way things work and think “There must be a good reason for that.” But this way of thinking, when taken too far, means you can never fix your mistakes! If central banks have been making a mistake by smoothing interest rates, then we want to identify and correct that mistake.

In fact, I can think of one case where the Fed did change rates very quickly — in 2008. By the time Lehman went bankrupt in September 2008, the Bernanke Fed had already been cutting rates for a while, but had paused that summer at 2%. But when the Lehman moment hit, Bernanke acted decisively, cutting rates all the way to near zero immediately.

Few economists, I think, would argue that this was a bad decision on Bernanke’s part. And it leads very naturally to an argument of why the Fed might want to make big, abrupt interest rate moves — at least in some situations. When the economy is moving very rapidly in one direction, our information about its current state is almost certain to be out of date. When the economy was crashing in late 2008, it was almost a certainty that things were worse than the Fed knew at the time, meaning it made sense to be bolder with rate cuts.

If you’re paying close attention, you’ll recognize this as simply the flip side of the argument that Sack & Wieland (2000) make against sudden rate moves. Sack & Wieland assume that uncertainty/measurement error about the state of the economy runs symmetrically in both directions. In that case, you want to go slow, because the economy might be growing faster or slower (and inflation running higher or lower) than you realize. But if the uncertainty runs only in one direction, the calculus obviously flips. In late 2008, Bernanke wasn’t wondering whether the economy was doing bad or good — he was wondering whether it was doing bad or really, really bad. So with the risk all on one side of the equation, it made sense to make big rate moves.

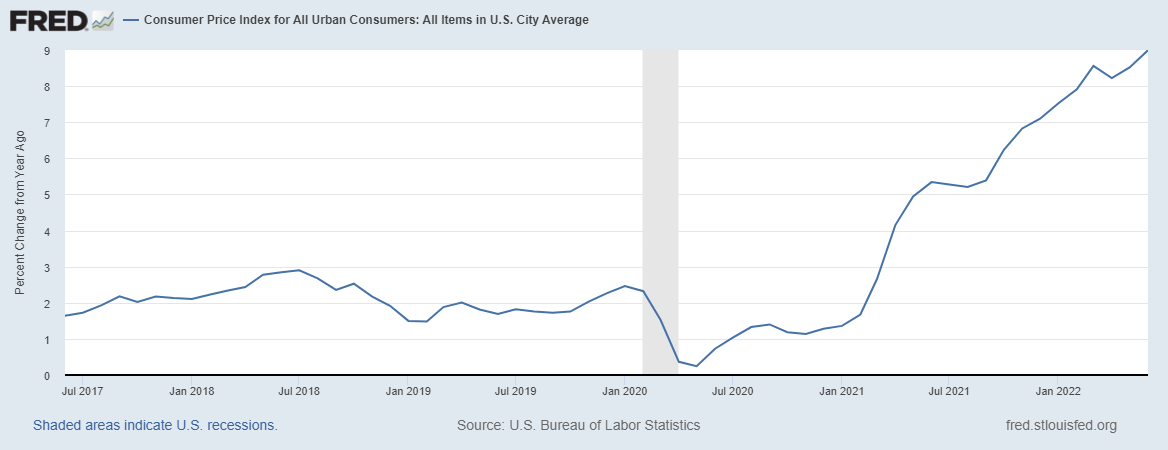

There are people arguing that the Fed faces a similar situation right now. Larry Summers, for example, continues to say that the Fed is behind the curve on inflation. Some voices from the banking sector have said the same. Their argument would seem to be bolstered by the fact that headline inflation has continued to accelerate in recent months, even as the Fed has stepped up its pace of rate hikes:

In other words, if this is a trend, then there are still forces pushing inflation higher and higher. In that case, the balance of risks is all on one side, and the Fed should be accelerating its rate hikes.

This is especially true if the Fed feels that it’s losing its credibility. A loss of credibility on inflation-fighting is a severe risk, because in the extreme case it might lead to a devastating hyperinflation that would be much worse than any recession.

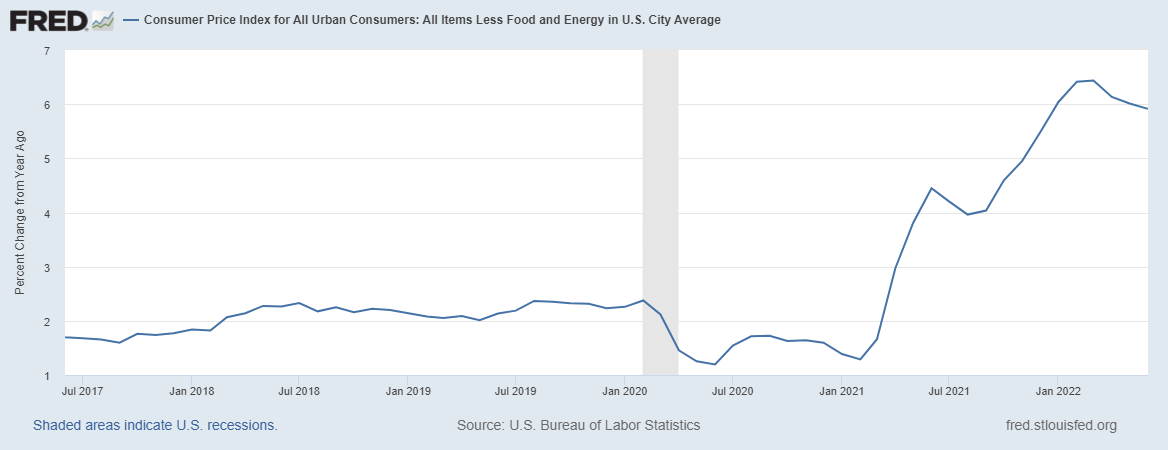

But then again, there are signs that the risks aren’t all on the inflationary side. When we look at core inflation, for example, we don’t see any acceleration over the last few months:

Inflation is still too high, but it doesn’t look like it’s going “up up and away”.

Meanwhile, as Brad DeLong and others keep pointing out, inflation expectations are hardly out of control — in fact, they’ve come down in recent months.

Meanwhile, signs of disinflation are proliferating — gas prices continue to drop, food prices are edging down, computer chips have switched from a shortage to a glut, and so on. And the economy may have just shrunk for the second quarter in a row.

So while a few months ago it really did look like the balance of risks were all on the inflationary side, now there might be risks on the recessionary side as well. Which would argue against bold, sudden rate hikes.

So there are good arguments both for and against a 200bp rate hike. I’ve semi-jokingly advocated a 200bp hike on Twitter, and I think it might be a good idea, but given the scattered signs of disinflation and recession, I don’t expect the Fed to actually do it. If inflation keeps accelerating, though, the Fed might give up on the idea that it’s transitory and start to worry about its credibility. If so, we might see a really big rate hike a few months down the line.

The ReadySetCrypto "Three Token Pillars" Community Portfolio (V3)

Add your vote to the V3 Portfolio (Phase 3) by clicking here.

View V3 Portfolio (Phase 2) by clicking here.

View V3 Portfolio (Phase 1) by clicking here.

Read the V3 Portfolio guide by clicking here.

What is the goal of this portfolio?

The “Three Token Pillars” portfolio is democratically proportioned between the Three Pillars of the Token Economy & Interchain:

CryptoCurreny – Security Tokens (STO) – Decentralized Finance (DeFi)

With this portfolio, we will identify and take advantage of the opportunities within the Three

Pillars of ReadySetCrypto. We aim to Capitalise on the collective knowledge and experience of the RSC

community & build model portfolios containing the premier companies and projects

in the industry and manage risk allocation suitable for as many people as

possible.

The Second Phase of the RSC Community Portfolio V3 was to give us a general idea of the weightings people desire in each of the three pillars and also member’s risk tolerance. The Third Phase of the RSC Community Portfolio V3 has us closing in on a finalized portfolio allocation before we consolidated onto the highest quality projects.

Our Current Allocation As Of Phase Three:

Move Your Mouse Over Charts Below For More Information

The ReadySetCrypto "Top Ten Crypto" Community Portfolio (V4)

Add your vote to the V4 Portfolio by clicking here.

Read about building Crypto Portfolio Diversity by clicking here.

What is the goal of this portfolio?

Current Top 10 Rankings:

Move Your Mouse Over Charts Below For More Information

Our Discord

Join Our Crypto Trader & Investor Chatrooms by clicking here!

Please DM us with your email address if you are a full OMNIA member and want to be given full Discord privileges.