Doc's Daily Commentary

Mind Of Mav

The Dawn Of A New Monetary Era – What Comes Next

As we discussed yesterday, we are entering a new monetary era, and central to understanding that comes with understanding inflation.

Let’s continue with part 3: The Dawn of a New Monetary Age

Quantitative Easing was always intended as a temporary measure that would help kickstart the economy. Central banks have dual mandates — keep unemployment low, and inflation within its target. That means that as the economy reaches full employment towards the end of the economic cycle, the central bank begins a monetary tightening to prevent cost-push inflation. Typically, this is done by raising interest rates, thereby making borrowing for individuals and corporations more expensive.

Monetary tightening is never politically popular, and many battles have raged between central banks and political leaders. But it is of the utmost importance in order to keep inflation in check. For this reason, legislation in most developed countries shields the central bank and its leadership from political interference.

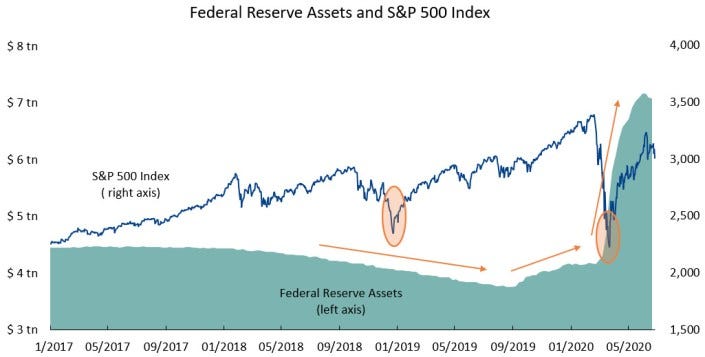

Let me show you how bad it has gotten:

Chart 6 — Federal Reserve assets, in trillions of dollars, and S&P 500 Index. The orange arrows represent the upward/downward trend of Federal Reserve assets; The orange ovals highlight the turning points of S&P 500 Index. The Fed suspended tightening its balance sheet and restored expansion to combat the global uncertainty triggered by the trade wars in September 2019; in March 2020, the Fed further expanded its balance sheets to dampen the market volatility caused by Saudi-Russian Oil War and COVID-19, bringing its assets over 7 trillion. Source: FRED Economic Data

The Fed started raising interest rates back in December 2015, but it wasn’t until 2018 that it started to unwind QE. This meant letting the bonds it was holding on its balance sheet mature, and perhaps even selling them in the open market. In turn, this would require the U.S. government to pay down some of its outstanding debt, or at the very least find new borrowers.

Not surprisingly, unwinding QE has the opposite effect of deploying QE. As can be seen in Chart 6, the stock market’s ascent stopped when news of the unwinding became public. President Trump, unhappy with this outcome, put immense pressure on Fed Chairman Jerome Powell to stop raising interest rates and restart QE. Ultimately, it appears that pressure worked.

In September 2019 the Fed began expanding its balance sheet. And while it insisted that this was an effort to stabilize financial markets and not economic stimulus, the outcome was the same and the stock market responded enthusiastically.

The Fed’s statements not withstanding, the bottom line is this: in the twelve years following the Great Recession, the Fed failed to shrink its balance sheet. With the economy at historically low unemployment, the Fed could not find a way, or was unwilling to bare the political price, of unwinding its allegedly temporary measure.

It is only fair to wonder why this is a problem. The Fed is a part of the U.S. government, so why should one part of the government pay back an outstanding loan to another part of the government?

This argument is most vocalized today by the proponents of Modern Monetary Theory (MMT). The theory suggests that in a modern economy, the notion of an independent central bank that controls the money supply is obsolete. Instead, the government can directly control the supply of money through its spending and taxation. In a recession, the government can cut taxes and increase spending by printing dollars — without borrowing from the public. As the economy reaches full employment the government can increase taxes and cut spending, and thus avoid demand-pull inflation.

In many ways MMT is the logical conclusion from a central bank that acts as a lender to the government, as it appears the Fed intends to do indefinitely. This is a sharp departure from the monetary policy that has governed developed economies for the past 40 years and was successful in taming inflation.

Put succinctly, the separation of fiscal policy from monetary policy is necessary for a stable economy. A pure MMT model requires politicians to strictly commit to spending money and cutting taxes only in bad times, and to increasing taxes and cutting spending in good times to avoid inflation. For an example of why this is a bad idea, look no further than the 2017 tax cuts — these are in direct contradiction with MMT’s suggestion that tax cuts take place only when unemployment is high.

While we are still far from a pure MMT model, permanent QE brings us closer to that reality. Unlike the QE that followed the Great Recession, it appears that much of this latest round has ended up in the hands of consumers and companies. There are a few reasons for this. For one, some of the QE money went directly to the Federal Government, who spent it on stimulus of various sorts including checks to individuals and the PPP program.

Another factor that could help the new QE money make it out to the public is the expansion of the program from treasuries to a wide range of fixed income securities, including bond ETFs and direct lending to companies.

Chart 7 — Commercial and industrial loans of all commercial banks (corporate lending), in trillions of dollars. The orange circle shows the peak of corporate lending in the week ending May 13, 2020. Corporate lending rose to $3.09 trillion in May 2020 as the Federal Reserve rolled out a $2.3 trillion loan program to facilitate PPP and other corporate loan programs. Source: FRED Economic Data, the Federal Reserve Data System

Still, even if the entire $3 trillion ends up in the hands of consumers, it is doubtful whether it is alone enough to cause inflation. Federal Reserve data suggests that U.S. households lost nearly $6.5 trillion of net wealth in Q1 alone. With unemployment in the teens, household wealth is bound to stay depressed for some time. Consumer spending has already dropped by nearly half a trillion dollars since March, and that’s with one-time stimulus checks and increased unemployment benefits that end in July.

All this however does not mean that we are out of the woods. Following the Great Recession, QE lasted six years, with ever larger programs. While $3 trillion may not be enough to cause inflation, an increase of the money supply by two or three times that amount very well could, especially if consumption returns to pre-COVID levels.

Should the Fed continue to supply the U.S. government with money on demand, the damage to the Fed’s independence would be a blow to the U.S. economy and jeopardize the role of the dollar as the global currency. Fiat money is based on trust, and if people believe that the Fed is no longer willing to do what it takes to keep inflation at bay, that could spell trouble for the dollar.

It’s certainly too early to eulogize the greenback, but unlike other periods of inflation in recent history, today there are other major contenders for the role of the global currency, namely the Euro and Chinese Yuan, or maybe even some type of Blockchain hybrid.

For the stability of the U.S. economy and the global standing of the U.S., it is imperative that the Fed resumes its role as a non-political and independent player. With U.S. government debt on the rise, there will never be a good time to end QE. However, the Fed must start planning just such an unwinding of its balance sheet well before the end of this new economic cycle. If it fails to do so we risk not only high inflation, but a loss of the very tool that has allowed the U.S. economy to prosper.

The ReadySetCrypto "Three Token Pillars" Community Portfolio (V3)

Add your vote to the V3 Portfolio (Phase 3) by clicking here.

View V3 Portfolio (Phase 2) by clicking here.

View V3 Portfolio (Phase 1) by clicking here.

Read the V3 Portfolio guide by clicking here.

What is the goal of this portfolio?

The “Three Token Pillars” portfolio is democratically proportioned between the Three Pillars of the Token Economy & Interchain:

CryptoCurreny – Security Tokens (STO) – Decentralized Finance (DeFi)

With this portfolio, we will identify and take advantage of the opportunities within the Three

Pillars of ReadySetCrypto. We aim to Capitalise on the collective knowledge and experience of the RSC

community & build model portfolios containing the premier companies and projects

in the industry and manage risk allocation suitable for as many people as

possible.

The Second Phase of the RSC Community Portfolio V3 was to give us a general idea of the weightings people desire in each of the three pillars and also member’s risk tolerance. The Third Phase of the RSC Community Portfolio V3 has us closing in on a finalized portfolio allocation before we consolidated onto the highest quality projects.

Our Current Allocation As Of Phase Three:

Move Your Mouse Over Charts Below For More Information

The ReadySetCrypto "Top Ten Crypto" Community Portfolio (V4)

Add your vote to the V4 Portfolio by clicking here.

Read about building Crypto Portfolio Diversity by clicking here.

What is the goal of this portfolio?

Current Top 10 Rankings:

Move Your Mouse Over Charts Below For More Information

Our Discord

Join Our Crypto Trader & Investor Chatrooms by clicking here!

Please DM us with your email address if you are a full OMNIA member and want to be given full Discord privileges.