Crypto Market Commentary

23 March 2020

Doc's Daily Commentary

The 18 March ReadySetLive session with Doc and Mav is listed below.

Mind Of Mav

Bitcoin, “Safe Havens”, & Unending Monetary Expansion

What the Internet did for speech, Bitcoin will do for money…¹

The above saying belies the fact that Bitcoin is also speech. The first Bitcoin transaction ever mined, broadcast at the height of the Great Financial Crisis, captures a powerful headline:

“The Times 03/Jan/2009 Chancellor on brink of second bailout for banks”²

Today, this message is secured by tens of thousands of computers comprising Bitcoin’s global network. Satoshi timestamped a critical moment at the start of a global monetary expansion often known as quantitative easing. Following the 2008 Great Financial Crisis, central banks around the world were in a dire position. Traditionally in times of trouble, central banks can lower interest rates to stimulate economic spending. However, even after cutting rates to zero or negative in 2008, the financial crisis would not abate.

So the central banks of the world turned to another monetary experiment of last resort. In the words of the Bank of England, “There’s a limit to how low interest rates can go. So when we needed to act to boost the economy, we turned to another method of doing so: we introduced quantitative easing.”³ Known by or closely associated with terms such as bailouts, QE, money printing, or balance sheet expansion, this is the practice of central banks buying assets with newly issued money. Today, even a decade after the financial crisis, monetary expansion has become a keystone of global markets.

Since 2008, trillions of newly issued dollars, yen, euro, yuan, etc. have been injected into the global economy. In the U.S., QE mainly means buying mortgage-backed securities and government Treasury bonds in exchange for newly issued dollars. The Federal Reserve buys these assets directly from a list of major commercial banks called primary dealers.⁴

What do central banks like the Federal Reserve hope to accomplish by mass buying government bonds? According to the Bank of England, “Large-scale purchases of government bonds lower the interest rates or ‘yields’ on those bonds… So QE works by making it cheaper for households and businesses to borrow money — encouraging spending. In addition, QE can stimulate the economy by boosting a wide range of financial asset prices.”³ As well as making it easier for households and businesses to borrow money, QE also encourages government spending.

To finance debt, governments issue bonds. Bond yields are supposed to reflect the risk of lending money to that institution, i.e. the higher the yield, the higher the risk premium. As an example, last decade Greece had a debt crisis that threatened to undermine the Euro monetary union. At one point Greece could only borrow at an extreme yield of 35%. Years later and despite still having a junk credit rating of BB-, Greek yields recently dropped below 1% on February 14. For context, the United States, which has a superior credit rating of AA+, yielded a higher rate of ~1.59%.⁵ After accounting for inflation, real bond yields are currently negative across the world and have dropped to historic lows in more recent days.

Imagine lending $10,264 for the privilege of receiving $10,000 in return.⁶ In a conventional world, countries like Greece should have paid a higher risk premium to borrow money. However, thanks to unconventional monetary policy, the opposite has occurred. Countries such as France and Japan are also able to issue nominal negative yielding bonds (before accounting for inflation). These negative returns compel other yield-hungry investors to buy riskier assets that offer a positive yield like Greek bonds.⁷ As of January there were over $10 trillion worth of negative yielding bonds, propped up by expansionary central banking.⁸

As bond yields and interest rates trend to zero or negative, people, businesses, and governments are encouraged to borrow money, spend more, and invest in riskier assets. Safe assets like bonds or cash savings accounts give a menial, or even negative, rate of return, so demand for other financial assets grows. U.S. equity valuations have soared as investors become dissatisfied with historically low bond and interest rate yields. In February, the P/E Ratio by Nobel economist Robert Shiller, which measures profit compared to valuation for the S&P 500, was near 1929 levels that preceded the Great Depression.

QE in one country can also cause a domino effect that leads to demand for currencies and equities of other countries (enabled by globalization and free movement of capital). According to Quartz in 2015, “…serious QE to lower yields in the eurozone is now steering investors toward Swiss assets”. The Swiss national currency, the franc, also has a historical affinity for being a so-called safe haven asset. This status began when the country preserved a gold standard amid the Great Depression. At the time, international investors flocked to the franc “as other continental currencies fell like dominoes”.⁹ However, a strong currency can harm aspects of a national economy such as equity markets, tourism, and manufacturing.

To dampen outsize safe haven franc demand, the Swiss National Bank has done three things to purposely devalue its currency after breaking its gold standard in 2000:

- Significantly expanded its balance sheet, continuously increasing new currency supply.

- Imposed negative interest rates, making it more expensive for investors to hold the currency.

- Publicly warned that the currency is “significantly overvalued.”¹⁰

In spite of all of these measures, the Swiss franc has appreciated against the Euro while experiencing upward volatility amid the Greek debt crisis.

The SNB’s monetary expansion involves directly purchasing American assets. In this strange global dynamic, monetary expansion in Europe drives demand for Swiss assets then Swiss monetary expansion drives demand for American assets. As part of its balance sheet expansion, the SNB has significantly increased its U.S. dollar holdings to a value of ~$267 billion.¹¹ The SNB also owned $94 billion worth of U.S. stocks such as Facebook and Apple, components of the S&P 500 referenced above, as “a result of the SNB’s huge currency interventions over the past decade to stem the franc’s rise.”¹²

Similar to the Swiss franc, the Japanese yen has been known in recent history as a safe haven currency.¹³ To also counteract the strengthening yen’s harmful effect on equities, tourism, and manufacturing, the Bank of Japan pioneered monetary expansion. By definition, new money supply dilutes the value of all existing money stock. If the “safe haven” demand is strong enough, value can continue to increase, however. So as U.S. Treasury bond yields fall to all time lows amid unprecedented monetary expansion, gold has risen in negative correlation.

2020 has been a turbulent year. Bad news can strike at any time, especially outside of traditional market hours. According to Bloomberg on the day that global coronavirus cases reached nearly 80k,¹⁴ “The SPDR S&P 500 ETF Trust, which tracks the benchmark gauge of American equities, has fallen an average of more than 1.2% at the open compared to the prior day’s close in the past three sessions amid concern over the spreading coronavirus.”¹⁵ Amid increasing uncertainty, traditional market investors may experience fear upon holding positions overnight or on weekends. There is only one asset class that trades 24/7, globally.

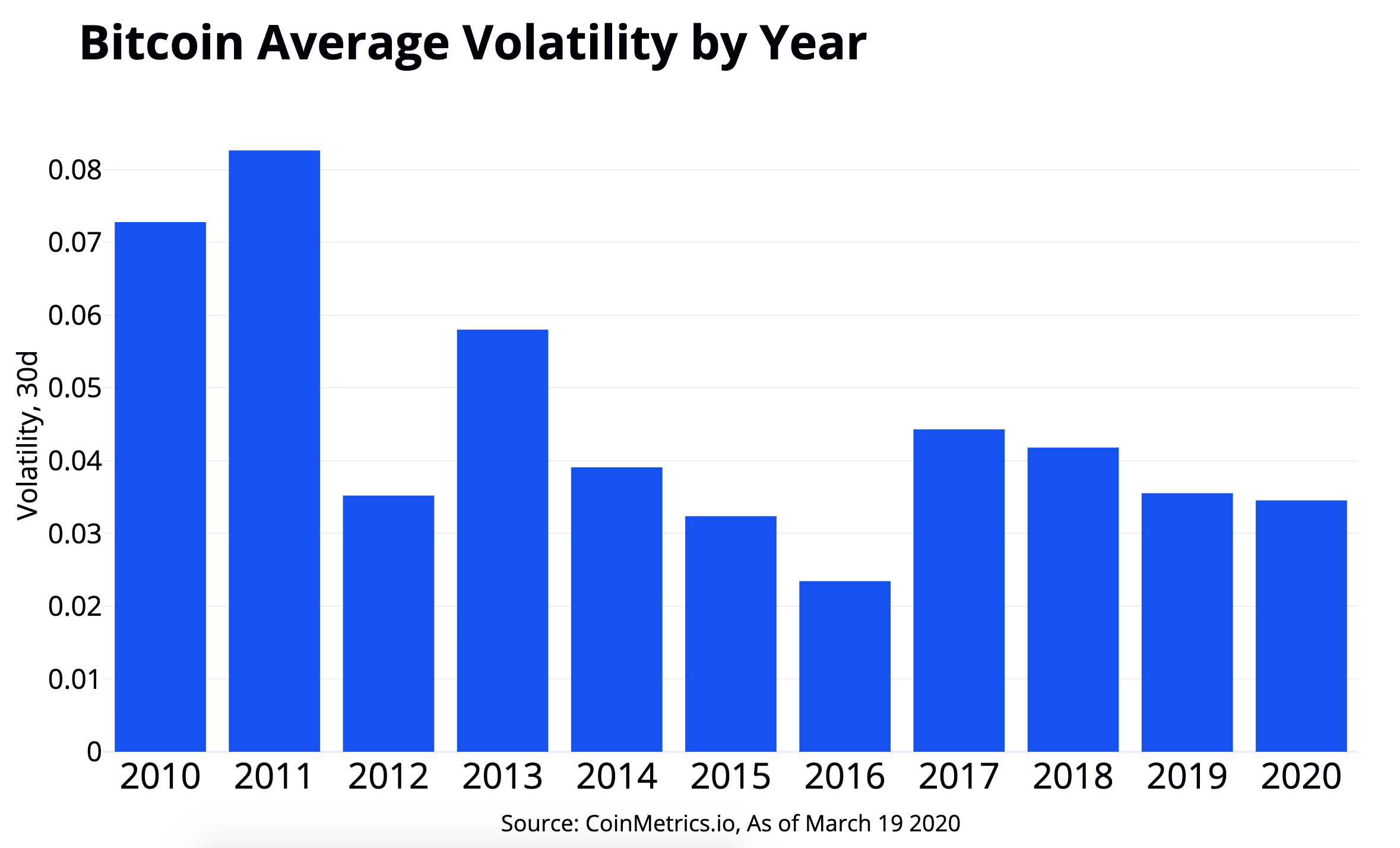

Correlation between gold and digital gold, seemingly in direct response to key geopolitical events, has driven considerable media interest this year. On the other hand, Bitcoin is significantly more volatile than gold, and such volatility may simply be a magnet for spurious correlation. Recently, Bitcoin behaves like an experimental tech stock, selling off alongside the Nasdaq as global markets shun risk assets. Past the technicals however, Bitcoin is fundamentally similar to gold in many ways. Bitcoin trades 24/7 globally, does not require a counterparty for transfer, and is uncensorable and scarce. Further, Bitcoin’s volatility appears to be declining over the years.

Central bankers of the world have been studying Bitcoin’s technological and economic potential. A recent Bank of England paper on Bitcoin suggests: “Price volatility may fall and payments usage increase if, in the future, a greater volume of speculation could be carried out outside the blockchain. Recent developments such as the evolution of cash-settled derivatives markets or the introduction of the Lightning Network could have profound consequences.”¹⁶

As evidence for the Bank of England’s thesis, the Chicago Mercantile Exchange has been reaching record levels of Open Interest for BTC cash-settled derivatives (although volumes have fallen in recent days amid the global selloff). For context, the CME is the largest financial derivatives exchange in the world, with billions of contracts traded per day for commodities such as gold and oil. As more speculation occurs beyond the Bitcoin ledger, its network may become more viable for digital payments. Bitcoin confirms a range of ~2–6 transactions per second on its globally distributed ledger.¹⁷ Users bid to complete a transaction via transaction fees, and median fees are currently ~30 cents.¹⁸

In parallel, another solution for Bitcoin’s scalability is growing: The Lightning Network is a technology for separate Bitcoin payment channels that periodically settle with the master ledger, freeing up space and allowing for instantaneous micro-transactions. The current median fee for a Lightning Network transaction is $0.00008.¹⁹ As a proxy for development, Lightning Network measures such as node and channels seem to indicate growing network participation.²⁰

Bitcoin’s digital gold thesis may yet evolve to find another niche in the global economy. In the meantime: all-time-low interest rates, surging government bond issuance, and unprecedented monetary expansion have become powerful economic forces. Macroeconomic risk has been obscured by this environment, as evidenced by equity overvaluations and low risk premiums for surging sovereign debt. During a protracted economic downturn, monetary and fiscal policy will be further tested to the limits. So as global fiat currencies like the franc, yen, etc. are supplied in increasing abundance alongside government bonds, will demand stay constant?

From the questions of unconventional monetary policy, Bitcoin presents an unconventional answer.

Endnotes

- Nick Szabo (Popular Science): “Like the Internet flattened global speech, Bitcoin can flatten global money’

- University of Miami Law Review: “Bitcoin is Speech”

- Bank of England: “What is quantitative easing?”

- New York Fed: Primary Dealers

- WSJ: Treasury Yields Hit New Lows, With 10-Year Settling at 1.127%

- Bloomberg Graphics: Negative Yielding Bonds

- Financial Times: Greek 10-year bond yield falls below 1% for first time

- WSJ: As Negative Yields Ebb, Making Money in Bonds Is Still a Slog

- Sotheby’s: The strong franc: the story of a safe-haven currency

- CNBC: Swiss National Bank: Franc ‘significantly overvalued’

- As of Feb. 2019, Trading Economics: Foreign Exchange Reserves, SNB: Foreign exchange reserves

- As of Nov. 2019, Bloomberg: SNB’s U.S. Equity Holdings Climb to a Record $94 Billion

- IMF: The Curious Case of the Japanese Yen as a Safe Haven Currency

- Johns Hopkins CSSE: Coronavirus COVID-19 Global Cases

- Bloomberg: Overnight Equity Declines Get Even Worse

- Bank of England Working Paper: Blockchain Structure and Cryptocurrency Prices

- Blockchain: Transactions per Second

- Coinmetrics.io

- 1ML.com: Lightning Network Statistics

- Disclaimer: According to bretton: “Lightning Network views tend to be the view of the network from a single node, or small selection of nodes. They are not complete views of the network.”

Press the "Connect" Button Below to Join Our Discord Community!

Please DM us with your email address if you are a full OMNIA member and want to be given full Discord privileges.

An Update Regarding Our Portfolio

RSC Subscribers,

We are pleased to share with you our Community Portfolio V3!

Add your own voice to our portfolio by clicking here.

We intend on this portfolio being balanced between the Three Pillars of the Token Economy & Interchain:

Crypto, STOs, and DeFi projects

We will also make a concerted effort to draw from community involvement and make this portfolio community driven.

Here’s our past portfolios for reference:

RSC Managed Portfolio (V2)

[visualizer id=”84848″]

RSC Unmanaged Altcoin Portfolio (V2)

[visualizer id=”78512″]

RSC Managed Portfolio (V1)