Doc's Daily Commentary

Mind Of Mav

CBDCs Revisited – Are They Doomed To Fail?

As a result of innovations based on blockchain, and other decentralized software systems, hundreds of new currencies have emerged. These solutions aim to address a wide variety of deficiencies of legacy financial systems, which often rely on digital technologies dating back to the 1960s, and in some cases are still analog.

Not to be outdone by cryptocurrencies and smart wallets, central banks around the world announced their own efforts to improve the capabilities of their respective national currencies.

However, it has become increasingly obvious that policy and design discussions under the label of CBDCs do not indeed address the most obvious problems that users – and those left out – of legacy financial systems, experience.

The following observations address the largest elephants in the room of otherwise vacuous CBDC discussions: the observable downsides of digital fiat, as well as the increasing adaption of solutions mitigating or solving these.

Problem 1: Financial Surveillance

Question: Will CBDCs reign in the current wholesale surveillance of all digital financial transactions, and restore financial privacy?

To date, with few exceptions financial transactions involving digital forms of government-issued fiat currencies involve the disclosure of personal identifiable data of the recipient and sender, regularly sharing this information with a number of intermediaries retaining copies – often for undisclosed purposes.

This wholesale surveillance of financial transactions is at the core a result of regulation purportedly aimed at bad actors wanting to use the financial system for the purpose of money laundering or other nefarious activities.

As extensively documented and widely reported (see this Economist article) AML measures have largely failed to mitigate illicit financial activity. However, intermediaries keep exposing sensitive information to a wide variety of data brokers, and their outdated systems are susceptible to criminals gaining access to slews of poorly secured databases.

47% of Americans experienced financial identity theft in 2020 (src).

While many CBDC discussions in democratic societies make mention of the necessity of privacy-preserving features, these are usually followed up by remarks that AML regulations will still need to be followed. More egregious though is the weaponization of fiat financial systems by totalitarian governments which persecute their own citizens, including for such ‘crimes’ as publicly disagreeing with the party line in social media.

Digital privacy – including financial privacy – is readily available via encrypted communication, and peer-to-peer value transfer solutions. However, the latter quality can scarcely be expected to be implemented in CBDCs by governments eager to control their population. Equally obvious are the effects of the implementation of actual digital bearer instruments to the next problem.

Answer: The implementation of CBDCs, as discussed by most central banks to date, will very likely further erode personal financial privacy, and allow totalitarian governments to increase financial controls.

Problem 2: Loss of Purchasing Power

Question: Will CBDCs mitigate against the loss of purchasing power of fiat currencies?

Throughout history, nation-states have continuously increased the supply of government-issued fiat currencies both in physical and digital form, frequently with devastating externalities to their own citizens unfortunate enough to be limited to use of that currency.

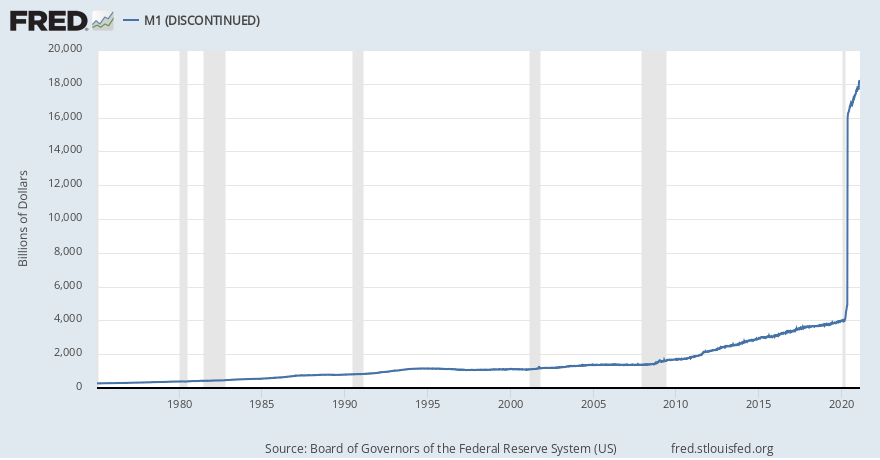

In January 2020, the US Federal Reserve reported fiat money supply of $4 trillion, this number skyrocketed to $6.7 trillion by January 2021 – an increase of more than 30% within twelve months. Incidentally the Federal Reserve abruptly stopped reporting on M1 money supply on February 1st 2021.

Setting the decades-long systemic inflation of assets – in particular the housing, education, and stock market – aside, the loss of purchasing power of fiat currencies has long been promoted as a feature by central banks.

This somewhat bizarre assertion – which deserves its own discussion, has now reached a high point of absurdity, expressed in “negative interest rates” and yields for fiat locked in money market accounts and certificate of deposits falling below even the most charitable inflation definitions. In the United States the latter group – for simplicity referred to in here as ‘M2’ – in aggregate now exceeds the amount of all outstanding mortgages.

The creation of additional fiat currency by commercial banks for existing real estate, can readily be prevented by the introduction of nearly fully automated lending products benefitting mortgage seekers and capital holders alike.

Setting the distortion of market forces by government intervention via tax-deductible interest rate payments, and student loans without default option aside, this elimination of money creation for non-productive activity may further slow down the inflation of real estate which year-over-year priced out one percent of the US population, while creating a mirage for home owners that their often only asset had increased in value.

This conflation of price and value – observable in other sectors of the economy, is further feeding yet another cottage industry of brokers and escrow agents, adding little or no value to productive activity, and are readily replaceable by decentralized software solutions. The elimination of middlemen from the process of loan origination and securitization can ultimately reign in the systemic inflation of asset classes, while limiting the continued debasement of government-issued currencies.

But new entrants into the space are competing with deputized government agencies under the misleading label of ‘commercial banking’ which are empowered to create money from nothing with every new home loan for pre-existing real estate. Moreover, given the outsized influence of the financial services sector over the legislative branches of government, it seems unlikely that this unfair advantage will be curtailed in any meaningful way before the foreseeable bursting of the current asset bubbles.

The latter added almost the entirety of publicly traded companies using low or zero-interest loans to compete with stock buyers by buying back their own stocks.

The continued efforts of central banks to position CBDCs as advancement from analog systems via labels such as ‘Digital Dollar’, requires us to point out the obvious: fiat currencies have been predominantly digitally native for decades, and are stored and moved as bytes. A meaningful departure from the current state of banking technology would necessary have to include the creation of digital bearer instruments which would not depend on the use of middlemen.

However, this would effectively void the need for demand deposit accounts (“checking accounts”) entirely, as the technical limits of bytes are based in physics. In simple terms: any user would be able to move bytes labelled as fiat currency entry ($) from a yield-bearing state to the recipients yield-bearing account.

With that the ability of financial service providers to extract fees from the movement of bytes would vanish, after all users tend to not put stamps on their emails. This, somewhat obvious conclusion, even made it into several CBDC research papers, and promptly caused the commissioning central banks to halt any development of a CBDC, realizing that fees for payments today comprise on average 30% of commercial bank revenues, these institutions would largely seize to exist.

Answer: CBDCs will not reign in the loss of purchasing power for users of government-issued fiat currencies.

Problem 3: Banking the Unbanked

Will CBDCs facilitate access of currently unbanked citizens to the financial system?

While most CBDC discussions stress the importance of inclusion of the ‘unbanked’ to the financial system, they regularly fail to address the true reasons why citizens do not maintain bank accounts. Despite the fact that legal tender laws point to the obvious public nature of fiat currencies, governments regularly deputize commercial entities to administrate and intermediate the use of national financial systems.

This extension of government powers to otherwise commercial entities has in some cases led to the outright confiscation of funds custodied by banks. These ‘bank bail-ins’ have been used in Cyprus, depositors with more than 100,000 euros to write off a portion of their holdings. Although the action prevented bank failures, it has led to unease among the financial markets in Europe over the possibility that these bail-ins may become more widespread, while eroding consumer trust in banks in general.

Setting these extreme examples aside, the fact that financial institutions are empowered to impose their own conditions on the use of the banking system has led to a systemic discrimination against consumers that are deemed to be unprofitable, and in some cases do not conform with the moral framework of banking executives.

The largest group of unbanked however, is comprised of individuals unable or unwilling to pass stringent anti-money laundering procedures often charitably labelled as ‘know-you-customer’ requirements.

Tellingly, that term even appears in quotations within the secretly extended legal requirements for – what must otherwise be considered – an invasion of financial privacy. CBDCs discussions offer little hope for the two billion unbanked citizens, most of which do not even possess government credentials.

Answer: CBDCs will not ‘bank the unbanked’ in a meaningful way.

Conclusions

Like the Royal Mail Ship Titanic, fiat currencies have hit the cold reality of an unmoving iceberg. And, current CBDC design papers avoid the most important leaks of government issued fiat currencies, resulting in mostly meaningless discussions around the specifics of their implementation. Hundreds of experiments have shown that digital units of accounts can be moved an settled with finality instantly. And, a one hundred billion dollar peer-to-peer digital lending market proofs that databases and their custodians are not needed. Fiat money in digital form has always been in a constant state of lending. Digital bearer instruments can reliably remove middlemen – such as commercial banks – and finally allow rightful owners of currency to determine who they want to entrust with their funds.

Aside from the language of value, money is a technology to facilitate commercial activity. We should no more go back to paying for phone calls by the minute, than going back in time before the invention of digital bearer instruments. – What’s in your wallet?

The ReadySetCrypto "Three Token Pillars" Community Portfolio (V3)

Add your vote to the V3 Portfolio (Phase 3) by clicking here.

View V3 Portfolio (Phase 2) by clicking here.

View V3 Portfolio (Phase 1) by clicking here.

Read the V3 Portfolio guide by clicking here.

What is the goal of this portfolio?

The “Three Token Pillars” portfolio is democratically proportioned between the Three Pillars of the Token Economy & Interchain:

CryptoCurreny – Security Tokens (STO) – Decentralized Finance (DeFi)

With this portfolio, we will identify and take advantage of the opportunities within the Three

Pillars of ReadySetCrypto. We aim to Capitalise on the collective knowledge and experience of the RSC

community & build model portfolios containing the premier companies and projects

in the industry and manage risk allocation suitable for as many people as

possible.

The Second Phase of the RSC Community Portfolio V3 was to give us a general idea of the weightings people desire in each of the three pillars and also member’s risk tolerance. The Third Phase of the RSC Community Portfolio V3 has us closing in on a finalized portfolio allocation before we consolidated onto the highest quality projects.

Our Current Allocation As Of Phase Three:

Move Your Mouse Over Charts Below For More Information

The ReadySetCrypto "Top Ten Crypto" Community Portfolio (V4)

Add your vote to the V4 Portfolio by clicking here.

Read about building Crypto Portfolio Diversity by clicking here.

What is the goal of this portfolio?

Current Top 10 Rankings:

Move Your Mouse Over Charts Below For More Information

Our Discord

Join Our Crypto Trader & Investor Chatrooms by clicking here!

Please DM us with your email address if you are a full OMNIA member and want to be given full Discord privileges.