Doc's Daily Commentary

Mind Of Mav

The Two Reasons Traditional IPOs Are Terrible

As we’ve discussed, the Traditional IPO process is totally broken.

In essence, there are two principle problems with it: the pricing process, and the fees.

Today, we’ll dig into both. I promise it will be more exciting & informative than it sounds 😉

Let’s start with why the fees of IPOs are crazy.

Fees Fees Fees

I hate fees. Don’t you?

Well, imagine pouring your life into building your dream company, growing it to the point of being ready to publically list it, and then some guy in an Armani suit takes a huge chunk of your company equity just because.

That’s right. You don’t pay in cash to list on the stock exchange . . .

You pay in BLOOD!

. . . ok, ok.

I’ll admit, that’s a slight exaggeration. Mea culpa.

Still, when conducting a Traditional IPO, it’s no exaggeration to say that the fees are egregious.

Right off the bat, the company going public will give up a significant percentage of their equity to the bank underwriter. Seems like a pretty sweet deal for whatever bank underwriter gets picked to perform the IPO, right?

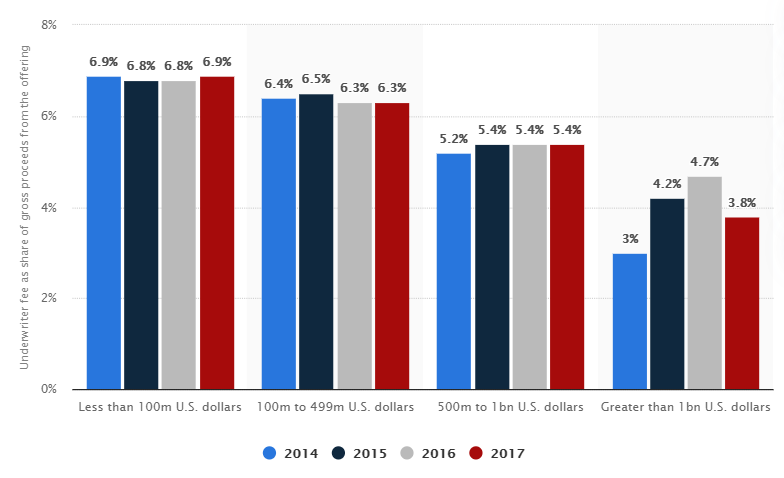

To underwrite a traditional IPO, banks charge 3-7% of the amount up for sale.

For example, if a company is selling $1B worth of equity, the bank can take in $30-70M for some paperwork. That’s a good chunk of cash!

You didn’t have to work 80+ hours a week for the last 5 years building the startup nor did you have to risk everything you had to make it work. You just had to sign some forms and shake some hands.

As a real-world example, when Facebook went public, it split 1.1 percent of the $16 billion raised in its IPO. That means the 33 investment banks that were hired to underwrite the offering were paid a cool $176 million to conduct the process.

The mind-boggling part is that Facebook, having a large cash position and therefore leverage to negotiate down the fees, only had to pay $176 million. Had they been forced to pay 7%, it would have cost them $1.12 billion just to be publically listed on the stock market . . . something that shouldn’t be so arbitrarily gatekept.

Thankfully, this is where SPACs start to show their value.

Fortunately for the company looking to go public, not only is a SPAC faster and less complicated of a process (a godsend for extremely busy startups who don’t have time to jump through hoops incessantly), SPAC IPO bank fees are in the same range.

According to Gig Capital, a SPAC expert:

The SPAC entity sponsors typically pay a 2% underwriting fee at the time of the SPAC IPO, with an additional 3.5% underwriting fee (i.e. based on the SPAC IPO size) paid by combined company at the completion of merger.

Needless to say, any process that is fairer to the company who put in the blood, sweat, and shares required to make an IPO possible in the first place should be given their fairest share.

Not to mention, a SPAC gives retail investors early-access to these pre-IPO companies, dramatically empowering their individual agency over the markets and vastly expanding their access to emerging industries.

After all, who is the real loser in a Traditional IPO?

Obviously, the company publically listing is forced to endure a small amount of pain for the promise of a large amount of reward, but the real loser here is the retail investor forced to eat the scraps off the floor.

For both the publically listed company and the retail investor, it’s a bad deal.

Meanwhile, the bankers eat their cake and pop their champagne.

Don’t worry, though . . .

It gets worse.

The Broken IPO Pricing Process

During an IPO, companies are incentivized to sell shares to investment bankers, their clients, and public market investors at the highest price possible, yet non-company investors are incentivized to buy the shares at the lowest price possible. Sounds like good ol’ supply and demand, right?

Sure, this difference in incentives should theoretically help to find a market equilibrium of price for the newly listed stock.

However, in practice, it often doesn’t.

Remember, bankers have much more experience in this process than the companies going public. It’s just like how a car salesman trains themselves every day to get you to buy a car for the highest price possible whereas you will likely only purchase a few cars in your lifetime.

When you walk into that car dealership, you are at the disadvantage, even if you think you can negotiate and haggle like it’s Shark Tank.

Now, I hear you.

Bankers and car salesmen have companies to represent and profits to make, and it is literally the job of investment bankers to price IPOs and raise capital as companies enter the public markets. They do this numerous times a month or year.

On the flip side, the founders of the company pursuing an IPO are likely to bring a company public only once in their life. This is their golden ticket & winning lottery number all wrapped into one, so they’re likely experiencing tremendous anxiety throughout the months and years it often takes to undergo the entire process. They are under immense pressure and constant scrutiny all while still having to devote a majority of their attention to running their business.

It would be an understatement to say that founders and their companies are at a disadvantage in the IPO pricing process.

This inherent disadvantage and lack of power, which has considerably widened over the years, has lead to IPOs being priced artificially low.

Whenever we see a traditional IPO, the stock price pops. It gets us tweeting. It gives us FOMO. Most importantly for the bank, it makes their clients (that bought the pre-IPO stock) richer.

Banks intentionally design this to happen.

I imagine them celebrating the IPO pop & wealth arbitrage like this:

Yet this arbitrage is daylight robbery of the very companies that go public.

This lack of balance in power leads to IPOs being priced artificially low, so investors can capture incredible upside return on their investments in a short period of time. This “IPO pop” has somehow become a barometer for how successful an IPO is.

Unfortunately, the company is the loser in this trade.

Ari Levy of CNBC nailed it when he wrote:

“For a second straight week, a tech company has more than doubled in value upon its stock market debut. Last week, it was Chinese cloud software developer Agora, which surged 150% in its first day of trading on the Nasdaq. And on Thursday, insurance-tech company Lemonade jumped 139%.

Tech IPOs have long been criticized for a process that lets investment bankers hand over underpriced stock to large public money managers, who often enjoy immediate and massive pops before ordinary investors are able to participate. Meanwhile, the issuing company ends up raising far less money than it could.

Over the past four months, with face-to-face meetings off the table, IPO roadshows have gone virtual. Management teams, with the help of bankers, are selling their story over Zoom rather than spending two weeks traveling to the money hubs of New York, Boston, Baltimore and San Francisco.

While they may be saving money on travel, they’re still leaving piles of cash on the table. Lemonade sold 11 million shares at $29 a piece, bringing in just over $300 million and giving new investors the $444 million difference, based on the closing price of $69.41. That’s a big deal for a company that had cash and cash equivalents of about $567 million before the IPO.”

In each of these scenarios, investment bankers and their clients more than doubled their money in a matter of minutes, yet the companies left hundreds of millions of dollars on the table. Seems like a one-sided trade, right?

That is because it is.

The success of an IPO should not be determined by how much the stock price appreciates once it is liquid, but rather by how much capital a business can raise without seeing a substantial drop in share price once the stock is trading.

So, there you have it.

IPOs are dying / broken / being disrupted by better models that are inherently better suited for the fast pace of today’s market and a more empowered retail investor.

In the next article, we’ll cover what those solutions are, and how they relate back to Solo Capitalism + SPACs.

The ReadySetCrypto "Three Token Pillars" Community Portfolio (V3)

Add your vote to the V3 Portfolio (Phase 3) by clicking here.

View V3 Portfolio (Phase 2) by clicking here.

View V3 Portfolio (Phase 1) by clicking here.

Read the V3 Portfolio guide by clicking here.

What is the goal of this portfolio?

The “Three Token Pillars” portfolio is democratically proportioned between the Three Pillars of the Token Economy & Interchain:

CryptoCurreny – Security Tokens (STO) – Decentralized Finance (DeFi)

With this portfolio, we will identify and take advantage of the opportunities within the Three

Pillars of ReadySetCrypto. We aim to Capitalise on the collective knowledge and experience of the RSC

community & build model portfolios containing the premier companies and projects

in the industry and manage risk allocation suitable for as many people as

possible.

The Second Phase of the RSC Community Portfolio V3 was to give us a general idea of the weightings people desire in each of the three pillars and also member’s risk tolerance. The Third Phase of the RSC Community Portfolio V3 has us closing in on a finalized portfolio allocation before we consolidated onto the highest quality projects.

Our Current Allocation As Of Phase Three:

Move Your Mouse Over Charts Below For More Information

The ReadySetCrypto "Top Ten Crypto" Community Portfolio (V4)

Add your vote to the V4 Portfolio by clicking here.

Read about building Crypto Portfolio Diversity by clicking here.

What is the goal of this portfolio?

Current Top 10 Rankings:

Move Your Mouse Over Charts Below For More Information

Our Discord

Join Our Crypto Trader & Investor Chatrooms by clicking here!

Please DM us with your email address if you are a full OMNIA member and want to be given full Discord privileges.