Doc's Daily Commentary

Mind Of Mav

2020: The Year Bitcoin Became An Institutional Sensation

A week ago, a prominent but very private financial newsletter author noted to clients that while he had never previously written about bitcoin, it was correct to say that institutional capital had now started to arrive in scale and that it would be churlish to pick a fight with it. Demand for bitcoin would now outstrip supply.

Bitcoin, he observed, would become an excellent metaphor for risk appetite in 2021 as a result. Less than a week later, Coindesk confirmed that UK-based asset manager Ruffer had accumulated some £550m of bitcoin since November, representing some 2.7 percent of the firm’s AUM. Ruffer’s move is now being widely interpreted as the beginning of a major portfolio diversification trend into bitcoin. It seems institutional money can no longer afford to ignore it. The crypto community is understandably overjoyed. Price moves since certainly could be indicating some sort of pragmatic acceptance of bitcoin in investment circles: © Courtesy of Coinmarketcap.com So have these institutions gone mad? Or are things genuinely different now? If they are, we think it all comes down to four key factors.

1. Bitcoin’s asset class status Whether critics like it or not, bitcoin’s status as an asset class is now much harder to dispute.

Yes, the cryptocurrency remains relatively useless as a medium of exchange outside of the dark markets. But it’s no longer clear whether that really matters. Bitcoin’s value has instead become linked to something more profound: its incapacity to go to zero despite having no central point of support or guarantor. This, we would argue, is a function of two key elements: a) too much-vested capital in the system to actually let it go to zero and b) enough shorts in the system to ensure short-covering at zero would inevitably be supportive. But it is also a function of another important phenomenon: the emergence of a competing tax authority to that of the state in the shape of the hacker.

This is important because the longstanding economic argument against bitcoin as an effective store of value has always been that fiat money is ultimately stabilized by the state’s capacity to demand taxes in its own currency. As was noted by Dealbook in 2013, “money is inevitably a tool of the state” and “no private power can raise taxes or pass laws to unwind monetary excesses”.

In 2020, however, that doesn’t seem quite right. Private “hackers” routinely raise revenue from stealing private information and then demanding cryptocurrency in return. The process is known as a ransom attack. It might not be legal. It might even be classified as extortion or theft. But to the mindset of those who oppose “big government” or claim that “tax is theft”, it doesn’t appear all that different. A more important consideration is which of these entities — the hacker or a government — is more effective at enforcing their form of “tax collection” upon the system. The government, naturally, has force, imprisonment, and the law on its side. And yet, in recent decades, that hasn’t been quite enough to guarantee effective tax collection from many types of individuals or corporations.

Hackers, at a minimum, seem at least comparably effective at extracting funds from rich individuals or multinational organizations. In many cases, they also appear less willing to negotiate or to cut deals. In an increasingly polarised world where a near majority of people don’t recognize the legitimacy of their governments, a bitcoin enthusiast might legitimately question what really constitutes legal extortion anyway? When established norms are in flux, everything becomes a matter of perspective and it would be irresponsible for fiduciary agents to bet on only one horse.

2. Bitcoin fought the law and the law won.

For a long time, institutional investment in bitcoin was hampered by strict investment mandates and regulatory compliance. Now that bitcoin has been formally recognized by many regulators, and regulated accordingly, this issue is far less of an obstacle than it used to be. We used to argue that bitcoin’s submission to authority was indicative of the core system’s superiority. If bitcoin wanted to play with the big boys it would have to also play by the rules they were governed by, and in so doing give up on its status as a renegade system. But there may be an important counterpoint we failed to consider. In bowing to regulation bitcoin abandoned its key “censorship-resistant” attributes, but it also paved the way for large-scale institutional investment. And that arguably is more important than temporarily bowing to the rules of the land.

As with ESG investing, once you command sizeable institutional money, you have the power to influence the rules themselves through the threat of divestment. In bitcoin’s case, that might include changing the rules to favor censorship-resistant forms of money. If you consider institutional flows into bitcoin as a form of ideologically-motivated divestment from fiat you can see they’re worth paying attention to.

3. Bitcoin’s volatility is a useful metric

In 2020, Bitcoin’s volatility factor has not gone away and remains bitcoin’s biggest nemesis with respect to wider public adoption (especially as a form of money). But from a trading and asset perspective, there is some justification in embracing the idea that bitcoin’s volatility is also an important window into market forces that are otherwise being suppressed. Central banks, whether rightly or wrongly, have worked hard to eradicate volatility from the financial system at the cost of ballooning balance sheets and centralized support for specific asset classes. A decisive move by institutional money out of central bank systems and over to bitcoin stands to turn any related volatility into a measure of that suppression. They say don’t fight the Fed because it will always win thanks to its infinite arsenal of cheap money.

The notion is based on the premise that cheap money is preferable to all else. But if you’re an institution looking for a healthy rate of return, your institutional objective is to protect investor capital against things such as negative interest rates. The fact institutions see bitcoin (in some ways the “hardest” of all currencies) as a mechanism to do that, is indicative of something important. The bigger question is how do they see bitcoin offering a return after the inevitable capital appreciation honeymoon they themselves trigger is over? The answer comes in the one thing that can’t be easily cultivated until bitcoin stops appreciating: a large and extensive debt capital market in which corporations can easily raise capital for real-world (not just digital) enterprise. The irony is it’s only once the price of bitcoin stabilizes that such a market can truly develop. And even after it does, some might argue why would anyone borrow in bitcoin rather than much cheaper fiat? Bitcoiners might retort that similar questions used to be asked of the offshore eurodollar markets. They mushroomed in size from the 1960s onwards regardless.

4. Bitcoin has successfully defied scrutiny

Scientists invite scrutiny because they know nothing is a better testament of success than having their inventions or discoveries defy continuous critique. Bitcoin may have started off as a belief system far removed from the scientific method, but in a roundabout way it has in the last 12 years invited as much, if not more, scrutiny than even Donald J Trump. As much as critics may loathe to admit it, the fact the system is still standing (if not flourishing by some people’s measures) constitutes something important.

Yes, bitcoin is yet to prove itself as more efficient or user-friendly than conventional fiat money. But it is no longer possible to deny its overall resilience. And since resilience was always part of bitcoin’s raison d’être that’s an important win for the would-be challenger system. All the more so if you consider that institutional money feels it can no longer afford to ignore it.

The ReadySetCrypto "Three Token Pillars" Community Portfolio (V3)

Add your vote to the V3 Portfolio (Phase 3) by clicking here.

View V3 Portfolio (Phase 2) by clicking here.

View V3 Portfolio (Phase 1) by clicking here.

Read the V3 Portfolio guide by clicking here.

What is the goal of this portfolio?

The “Three Token Pillars” portfolio is democratically proportioned between the Three Pillars of the Token Economy & Interchain:

CryptoCurreny – Security Tokens (STO) – Decentralized Finance (DeFi)

With this portfolio, we will identify and take advantage of the opportunities within the Three

Pillars of ReadySetCrypto. We aim to Capitalise on the collective knowledge and experience of the RSC

community & build model portfolios containing the premier companies and projects

in the industry and manage risk allocation suitable for as many people as

possible.

The Second Phase of the RSC Community Portfolio V3 was to give us a general idea of the weightings people desire in each of the three pillars and also member’s risk tolerance. The Third Phase of the RSC Community Portfolio V3 has us closing in on a finalized portfolio allocation before we consolidated onto the highest quality projects.

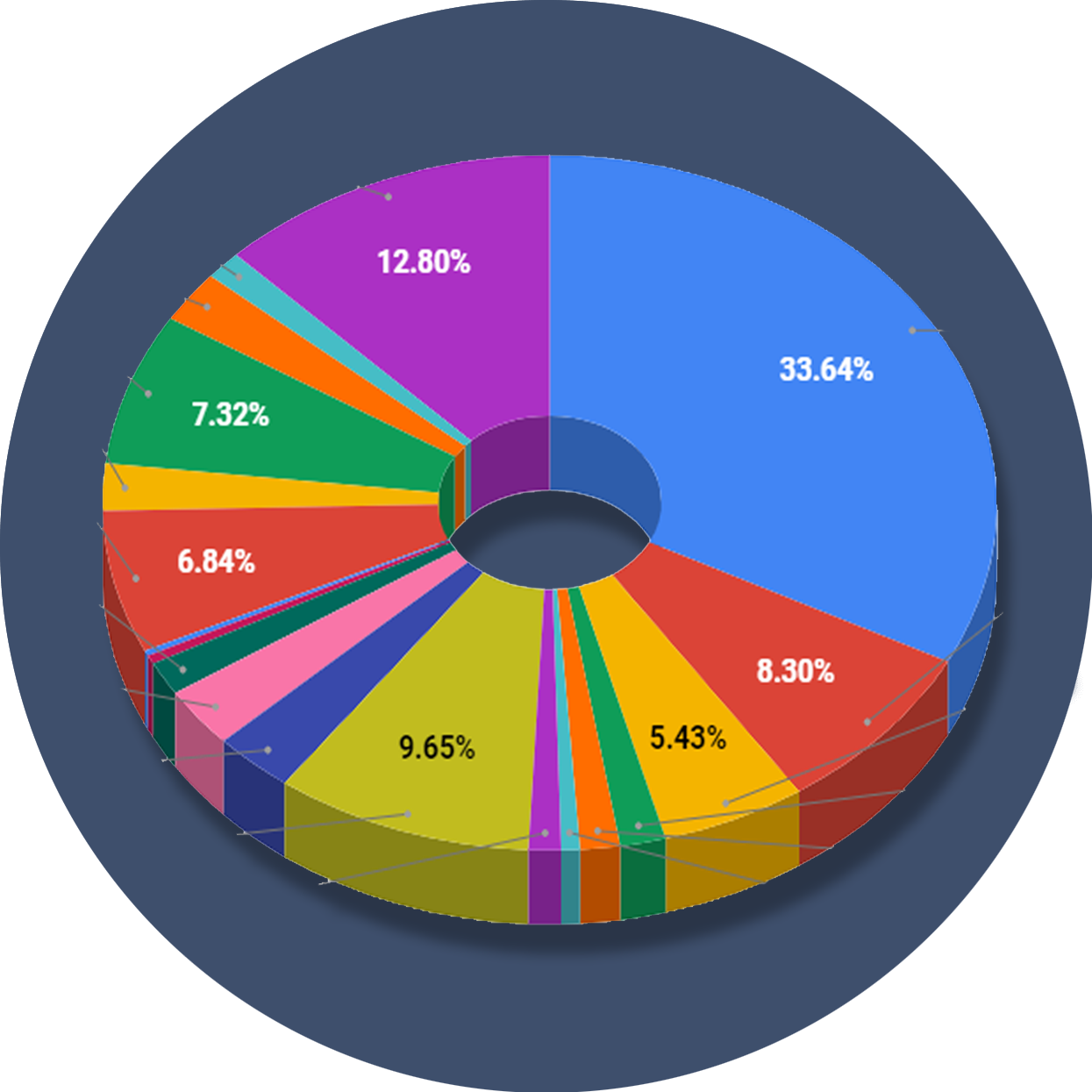

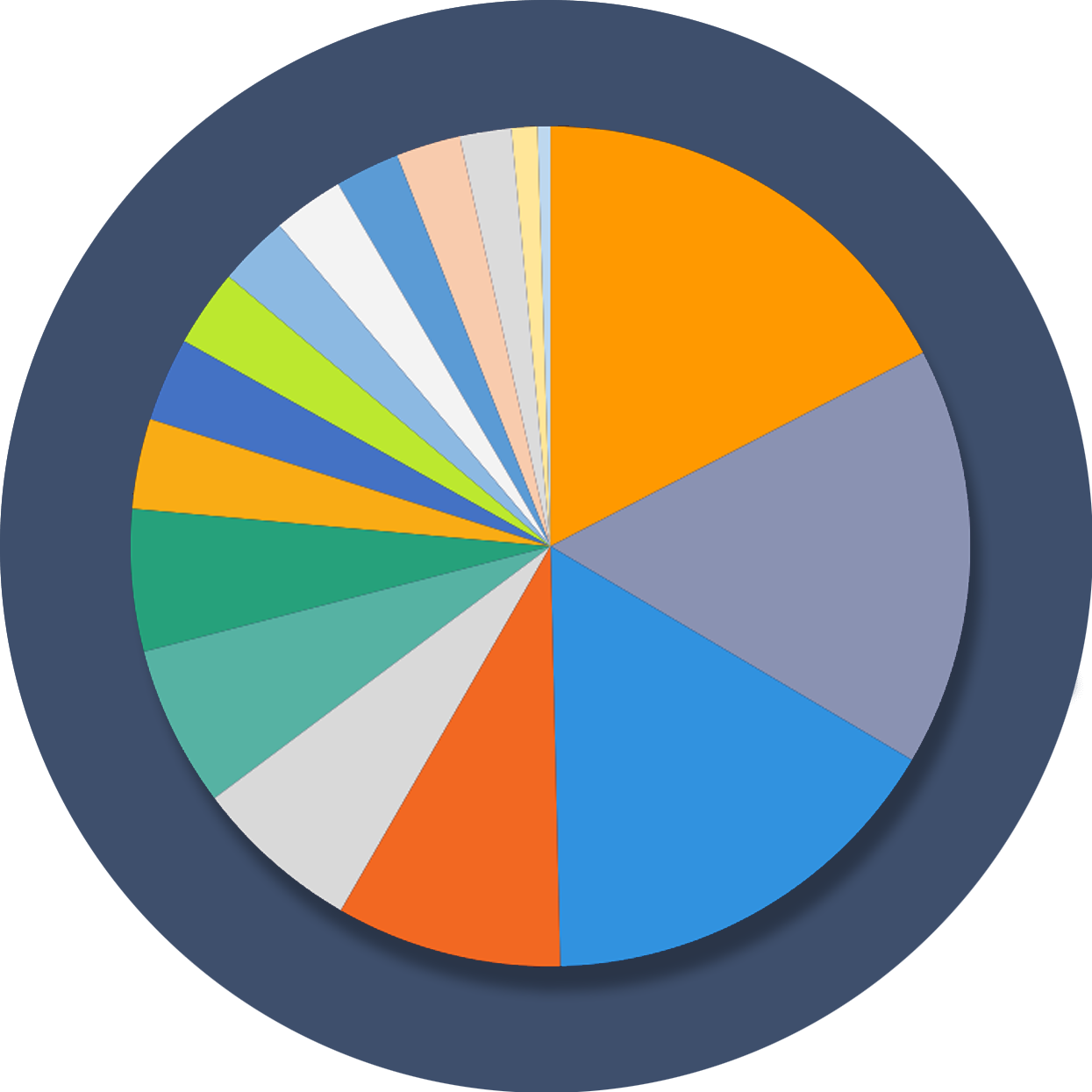

Our Current Allocation As Of Phase Three:

Move Your Mouse Over Charts Below For More Information

The ReadySetCrypto "Top Ten Crypto" Community Portfolio (V4)

Add your vote to the V4 Portfolio by clicking here.

Read about building Crypto Portfolio Diversity by clicking here.

What is the goal of this portfolio?

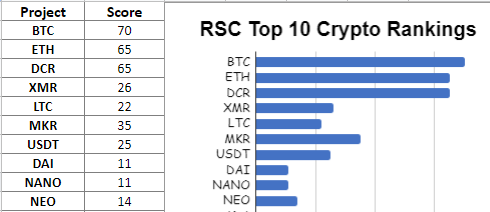

Current Top 10 Rankings:

Move Your Mouse Over Charts Below For More Information

Our Discord

Join Our Crypto Trader & Investor Chatrooms by clicking here!

Please DM us with your email address if you are a full OMNIA member and want to be given full Discord privileges.