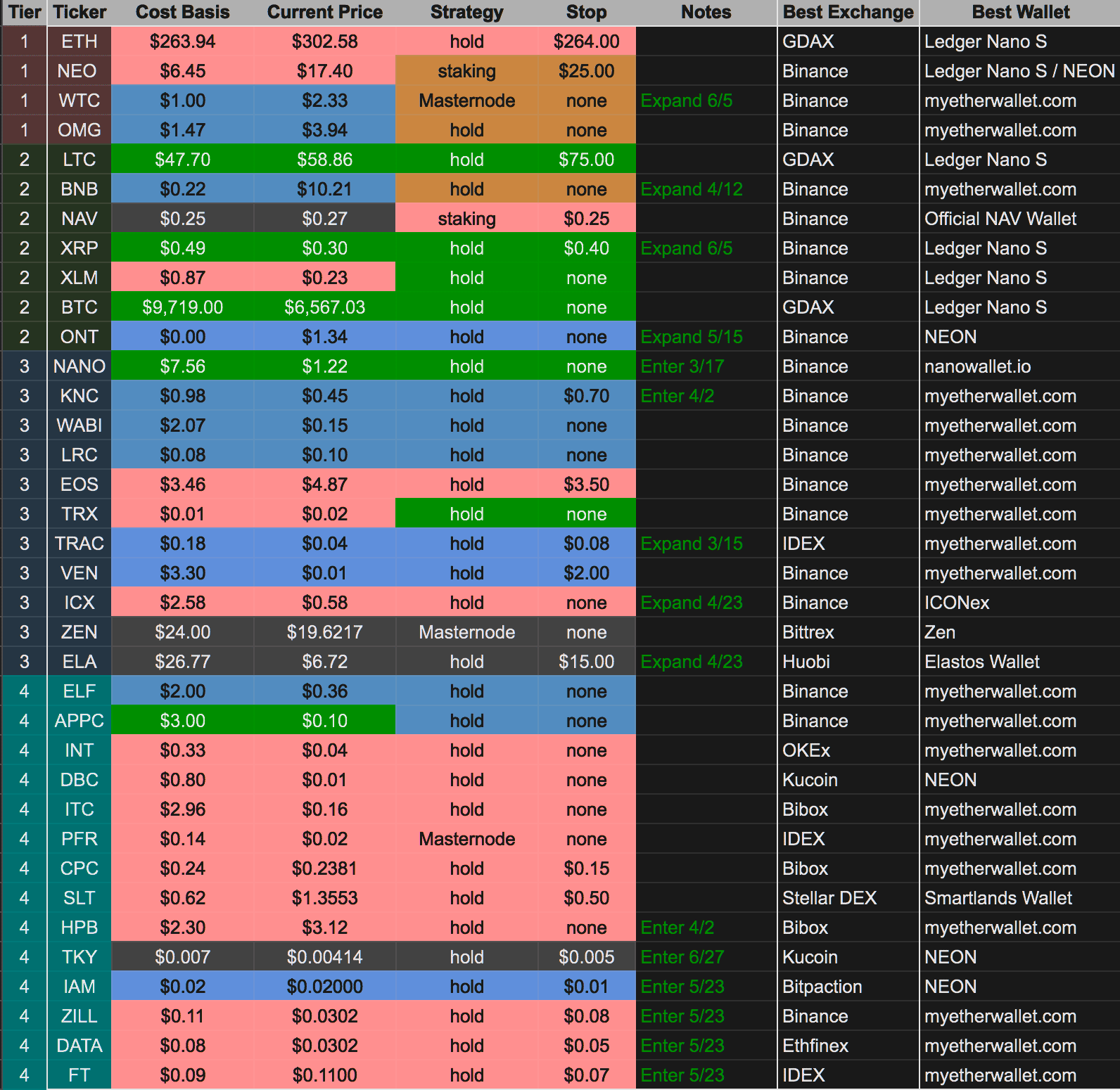

Crypto Market Commentary

19 June 2019

Doc's Daily Commentary

On 6/14 Doc conducted the first “House of Pain” coaching session, which is posted in the “Trade School” archive. Let me know if you have any interest in being a participant.

Our most recent “ReadySetLive” session from 6/19 is listed below.

Mind Of Mav

Will Facebook’s Libra Help The Unbanked Like They Claim? Probably Not.

So here’s the thing.

We don’t know what Facebook’s new Libra currency will actually be used for in the end. However, we do know that it’s being sold as a way to help the unbanked — it’s right there in the word “empower” in Libra’s one-sentence mission statement.

And we also know that Libra will not solve the problem of the unbanked.

From the white paper, here’s Libra’s “problem statement”:

All over the world, people with less money pay more for financial services. Hard-earned income is eroded by fees, from remittances and wire costs to overdraft and ATM charges. Payday loans can charge annualised interest rates of 400% or more, and finance charges can be as high as $30 just to borrow $100. When people are asked why they remain on the fringe of the existing financial system, those who remain “unbanked” point to not having sufficient funds, high and unpredictable fees, banks being too far away, and lacking the necessary documentation.

Here’s my “problem statement” to counter that one:

Facebook seems to be conflating the challenges of global remittances with those of financial services for the poor in the United States. It’s right there in the very serious footnotes from that paragraph: one uses US data, one uses global data. Both sources are haphazard, almost as if someone who’s never really thought about the unbanked googled up some stats at the last minute.

It doesn’t seem like this confusion is an accident.

Facebook seems to think that the unbanked face a systems challenge, to be fixed with private investment and remote engineers. But the people who actually study the problem of the unbanked, and who actually do something about it, treat it completely differently: as a sociological challenge, to address with education and local institutions.

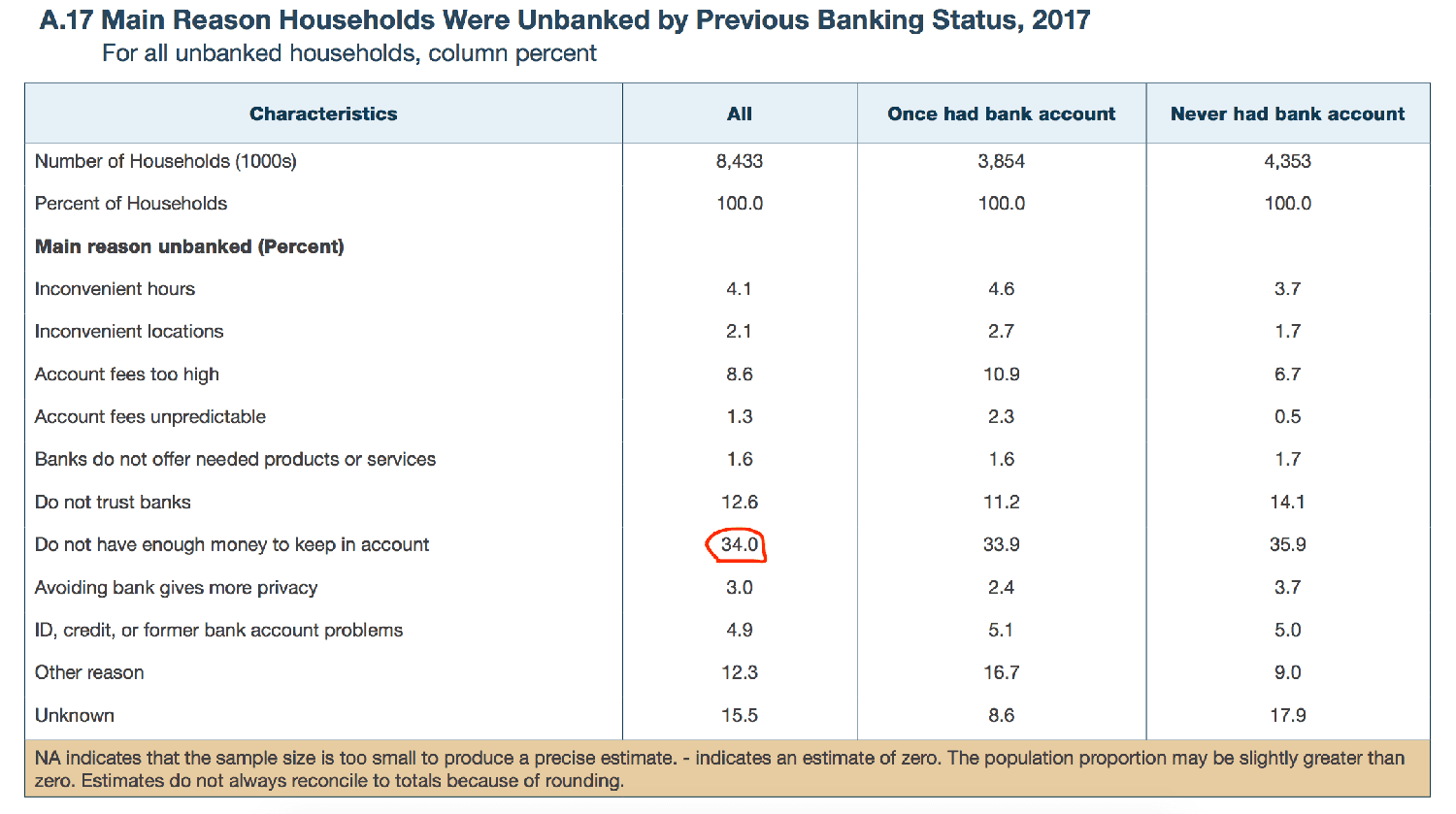

In the US, the Federal Deposit Insurance Corporation keeps the most comprehensive data on people who either lack bank accounts, or have a bank account but still use payday lenders or check cashers. The good news is the percentage of unbanked households in America has been dropping gently but steadily since 2011; the FDIC thinks this is most likely a straightforward consequence of economic growth.

The bad news is that in 2017 — the most recent of the FDIC’s biennial surveys — slightly more than half of the unbanked said they didn’t have an account because they didn’t have enough money to put in a bank. A third offered this as their first response. As you can see below, this is not the only answer, but it’s by far the most dominant answer:

The organisations that actually work on getting people into this banking system, most significantly Bank On in the United States, have identified two hurdles. First, existing consumer banks need to offer entry-level, low-fee checking accounts. Bank On has developed a list of standards for these accounts, and leans on banks, city by city, to offer them. And that’s the easy part.

The hard part is that, city by city, Bank On creates local coalitions of city governments, regional banks, and local nonprofits and social services. Actual people, following best practices that have been developed through experience in other cities, find locals where they are — kids at summer jobs, parolees at halfway houses, people receiving public benefits at the benefit offices — and work with them, over time, to walk through the sociological and administrative hurdles to getting a basic checking account.

“I don’t have enough money to open a bank account” isn’t a problem that can be solved by putting a bank account on the internet. It takes a lot of face-to-face conversations about what banking is, how it works, and why it’s an important tool for every household. For example, a recent pilot in New York City (paid for by Michael Bloomberg) found some success in offering a series of personal financial inclusion counselling sessions, almost like therapy.

This is personal, detailed, local work. It does not scale. It requires trust, and good relationships with civic authorities. To start with, there’s not much in our recent experience with Facebook that suggests they’d flourish as the senior partner in any initiative that demands personal, detailed, local work that requires civic trust. Nowhere in any research on the unbanked does it state that the US dollar is unsuited to the task of moving people into the formal financial system. So if you really want to help people, a brand-new currency seems like an awkward and convoluted way to do it.

And when you dig in to the details of how Libra is supposed to work, there’s nothing at all about how it will actually help the unbanked. There’s plenty about the Libra blockchain that’s not really a blockchain. There’s plenty about the Libra reserve that doesn’t seem to have read any history on how reserves work. There’s nothing about how Libra will lower fees to convert fiat cash into Libra money, which is both the essential challenge of consumer banking and an explicit part of Libra’s problem statement. Check-cashing places charge hideous fees, but they’re willing, on demand, to turn physical checks into physical cash, and physical cash into transfers.

If Facebook were willing to open local Libra conversion offices in low-income areas in Louisville, Kentucky, Lafayette, Louisiana and Rochester, New York — here’s a map of where Bank On is — it might actually help get people into the banking system. But it could also just do that without creating a new currency.

The most that Libra seems to have done is provide for what it calls a Social Impact Advisory Board. Tellingly, the board has exactly zero enumerated powers within Libra’s actual governance structure. Those are all held by members of the Libra Association Council, who can buy a share of votes in $10m increments. The social impact board can suggest nonprofits as council members, but this isn’t an enumerated power, and even if it works out, nonprofits can never add up to more than a third of the voting shares.

Libra’s Social Impact Advisory Board can, however, conduct research. And it can make recommendations on grants and social impact investments. This makes Libra a digital currency, with a governance structure that happens to run a foundation with a think-tank. Again, a foundation that encourages financial inclusion is something Facebook could have set up ten years ago, without creating a new currency.

It’s almost as if the people who set up Libra aren’t actually that interested in the unbanked.

Press the "Connect" Button Below to Join Our Discord Community!

Please DM us with your email address if you are a full OMNIA member and want to be given full Discord privileges.

An Update Regarding Our Portfolio

RSC Subscribers,

We are pleased to share with you our Community Portfolio V3!

Add your own voice to our portfolio by clicking here.

We intend on this portfolio being balanced between the Three Pillars of the Token Economy & Interchain:

Crypto, STOs, and DeFi projects

We will also make a concerted effort to draw from community involvement and make this portfolio community driven.

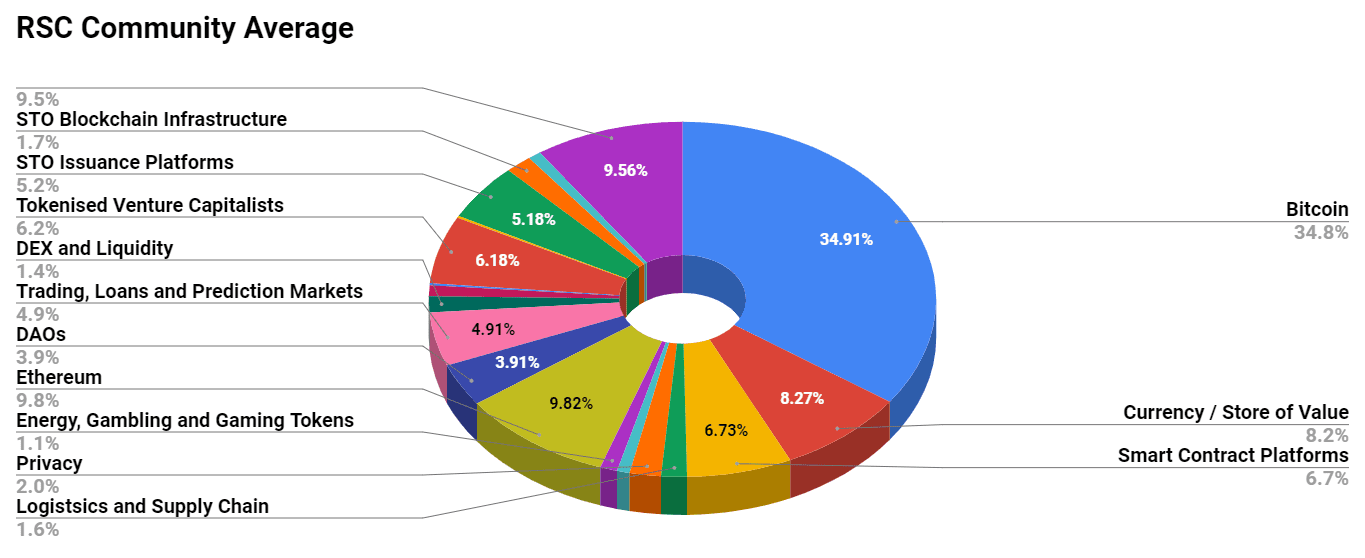

Here’s our past portfolios for reference:

RSC Managed Portfolio (V2)

[visualizer id=”84848″]

RSC Unmanaged Altcoin Portfolio (V2)

[visualizer id=”78512″]

RSC Managed Portfolio (V1)